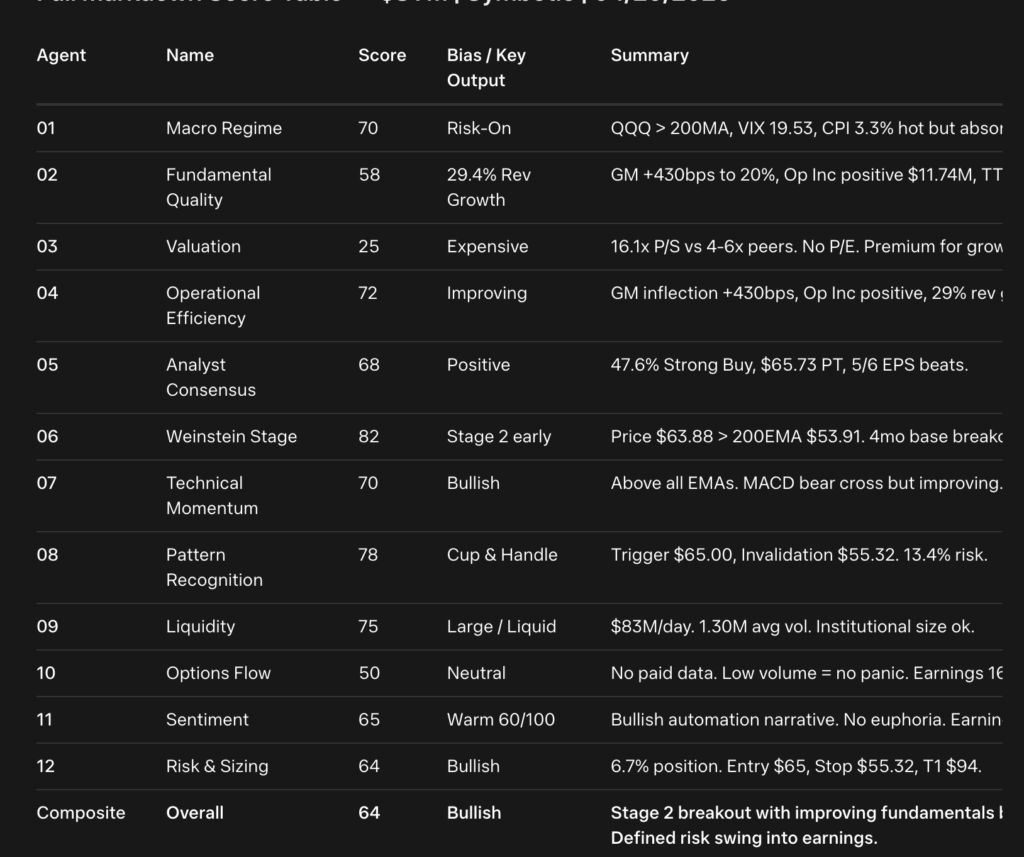

Symbotic is an industrial automation company building AI-powered robotics warehouses, with revenue inflecting +29.4% YoY to $630M in Q1 ’26 and gross margin expanding 430bps to 20% as operating income turned positive for the first time in 2 years.

The stock is in an early Stage 2 advance at $63.88, breaking out of a 7-month Cup & Handle base with 47.6% Strong Buy ratings, but still trades expensive at 16.1x sales with TTM unprofitable and earnings in 16 days as the next catalyst. Composite score 64/100 signals a bullish swing setup with defined risk at $55.32, driven by improving fundamentals and automation tailwinds, offset by valuation risk.

Symbotic grew Q1 ’26 revenue 29.44% YoY to $629.99M with gross margin expanding 430bps to 20.0%. Operating income flipped positive to $11.74M after 7 straight quarters of losses, showing operating leverage. TTM still -$48.96M, so quality inflecting but not proven.

At $63.88, SYM trades 16.1x TTM sales on $38.47B market cap with only $0.12 quarterly EPS. This is ∼3x richer than industrial automation peers at 4–6x P/S. Valuation prices in massive automation TAM capture and margin expansion that hasn’t hit TTM yet.

Gross margin inflected to 20.0% in Q1 ’26, up 430bps YoY, confirming scale on manufacturing. Operating income turned positive $11.74M for first time in 2 years. Revenue growth 29.44% YoY with expanding margins signals operational leverage kicking in.

SYM trades $63.88, 18.5% above rising 200-day EMA $53.91, confirming Stage 2 advance. The stock based 4 months between $46–$55 before April breakout on volume. EMA stack 20>50>100>200 shows bullish alignment.

Stage 2 Symbotic breaking Cup & Handle with first positive operating income and 430bps GM expansion. Risk-On macro + 47.6% Strong Buy ratings support continuation. Defined risk at $55.32 handle/50EMA.