Executive Summary

- EPS (Actual): $0.16 — beat consensus by $0.07, representing a ~78% positive surprise against the whisper number

- Annual Revenue Run-Rate: $491M total revenue (annual), with next quarter consensus sitting at $145M

- Gross Margin: 33.55% — a metric worth watching for operating leverage inflection signals

- Market Reaction: +43.87% single-session move, pushing market cap to approximately $830M

- Key Insight: After a trailing twelve-month EPS of -$0.46, a $0.16 quarterly print isn’t just a beat — it’s a narrative reset. The street is repricing the probability of sustainable profitability, and institutional desks that were underweight are now scrambling.

Earnings Overview

Here’s the thing about a 43-basis-point single-day move in a sub-$1B market cap name — it doesn’t happen on a modest beat. It happens when the market has been structurally wrong about a business for multiple quarters, and then reality arrives wearing a neon sign.

Pulling data from the Bloomberg Terminal and FactSet consensus models this morning, Digital Turbine’s Q1 FY2026 print landed with enough force to force a re-rating conversation across the technology services sector. The $0.07 EPS surprise — against a consensus estimate that had been drifting lower through Q4 2025 — tells us that sell-side models had not yet internalized the operational tightening that management telegraphed. That’s the kind of setup that creates alpha.

Contextualizing this within the broader 2026 macro environment: we are operating in a late-rate-cycle backdrop where the Federal Reserve has held rates at restrictive levels longer than most models anticipated. High-beta technology names, particularly those with uneven profitability histories, have been systematically punished in institutional portfolio construction. Digital Turbine carried exactly that stigma — a TTM EPS of -$0.46 that kept it off most quantitative screens and out of large-cap technology allocations. The Q1 2026 print is the first credible data point that suggests the cost restructuring and AI partnership pipeline are translating into actual margin recovery, not just management commentary. In a macro environment where growth is scarce and profitability is the differentiator, that shift in narrative carries disproportionate weight.

—

Financial Performance

| Segment/Metric | Current Result | Consensus/YoY | Strategic Signal |

|---|---|---|---|

| EPS (Q1 FY2026 Actual) | $0.16 | Consensus: $0.09 | Beat by $0.07 (~78%) | First meaningful profitability signal after -$0.46 TTM EPS; forces model revisions |

| Total Annual Revenue | $491M | Next Q Estimate: $145M | Sequential revenue stabilization critical; Q2 guidance adherence is the next catalyst trigger |

| Gross Margin | 33.55% | Below software sector median (~60-65%); YoY directional trend under watch | Margin expansion of even 200-300 basis points would materially re-rate the operating leverage story |

| Market Capitalization | ~$830M | Pre-earnings est. ~$577M (implied from -44% session delta); single-session re-rating of ~$253M | Float dynamics suggest short-covering amplified the move; watch for institutional accumulation in the 3-5 session follow-through |

| Next Quarter EPS Estimate | $0.09 (consensus) | vs. Q1 Actual of $0.16 | Conservative guide-down relative to print may reflect CFO transition uncertainty (Steve Lasher departure); also creates another potential beat setup |

—

Key Earnings Insights

- The AI Partnership Pivot Is Moving the Needle — Finally: Headlines referencing “new AI deals” driving a 15.3% move in a prior session, compounded by the full earnings print, suggest that Digital Turbine’s on-device software delivery infrastructure is being repositioned as an AI distribution layer. This is not a cosmetic pivot — if carrier and OEM partners are embedding AI-assisted app delivery contracts, the per-device monetization economics change structurally. The market is beginning to price in that optionality, which was entirely absent from prior consensus models.

- CFO Transition Is the Unpriced Risk in the Room: Steve Lasher’s departure, announced alongside an otherwise strong Q4/FY2026 report, introduces execution risk at the exact moment the company needs financial discipline to hold. In 28 years of tracking these transitions, a CFO exit during a turnaround is a yellow flag that institutional risk committees will note. The next 60-90 days of management communication — particularly interim CFO credibility — will determine whether this risk is absorbed or amplified into the stock price.

- 2027 Revenue Guidance Is the Real Anchor for Re-Rating: The market is not just reacting to a single quarter — it is repricing a forward multiple against a 2027 guidance framework that management introduced alongside the FY2026 results. For a name that spent multiple quarters without a credible forward narrative, the introduction of FY2027 revenue guidance signals management confidence and creates a framework for institutional analysts to build discounted cash flow models that previously couldn’t be constructed with any confidence. That guidance anchor, more than the Q1 beat itself, is what unlocks the next tier of institutional buyers.

—

The Practitioner’s Perspective

After 28 years of sitting through earnings cycles — including the dot-com unwind, the 2008 credit dislocation, and the 2022 rate shock that gutted unprofitable tech — I have developed a specific pattern recognition for what I call “inflection quarter” setups. Digital Turbine’s Q1 FY2026 print has several of the hallmarks.

>

The 43.87% single-session move is not, by itself, a signal to chase. What it is is confirmation that institutional positioning was structurally light — likely underweight or net short in quant-driven long/short books that screened out the name based on negative TTM earnings. When those desks are forced to cover and re-evaluate simultaneously, you get the kind of price action we saw today. The question for serious practitioners is not “did I miss the move” — it’s “is the re-rating durable?”

>

My read: the durability depends on two variables that the market will resolve over the next two quarters. First, gross margin trajectory. At 33.55%, Digital Turbine is operating below the threshold where software-comparable multiples become defensible. If AI deal economics bring even 150-200 basis points of gross margin expansion, the operating leverage story becomes self-reinforcing and the next multiple re-rating is justified. Second, the geopolitical angle on carrier and OEM partnerships deserves attention. On-device software distribution is subject to the same supply chain nationalism dynamics reshaping the broader semiconductor and software stack. If Digital Turbine’s OEM relationships are concentrated in markets facing trade friction — particularly in the Asia-Pacific corridor where Android device volumes are highest — that’s a tail risk that won’t show up in a single quarter’s beat but will matter to institutional risk committees building 18-month positions.

>

From a sector rotation standpoint, we are watching money rotate back into mid-cap technology names with a profitability proof point. Digital Turbine just produced that proof point. The institutional flows over the next 30 sessions will tell us whether this is a repricing or just a relief rally in a structurally impaired name. I know which one I’m watching for.

—

Frequently Asked Questions

What does APPS do?

Digital Turbine (Nasdaq: APPS) is a technology services company specializing in on-device software and application delivery solutions for mobile carriers and device manufacturers. The company’s platform enables wireless operators and OEMs to deliver applications, content, and digital media directly to consumers at the point of device activation and throughout the device lifecycle. Digital Turbine operates across advertising technology, content media, and app delivery segments, positioning itself as critical middleware between app developers and the hundreds of millions of Android devices activated globally each year. The company has been actively repositioning its platform to incorporate AI-driven delivery and monetization capabilities as of 2025-2026.

—

Why did APPS stock jump 43.87% after the Q1 2026 earnings report?

The move was driven by a significant EPS beat — Digital Turbine reported $0.16 per share against a consensus estimate of $0.09, representing a ~78% positive surprise. Coming off a trailing twelve-month EPS of -$0.46, the Q1 print marked a credible profitability inflection point that forced institutional desks to rapidly revise their models. The beat was compounded by the introduction of FY2027 revenue guidance and new AI partnership announcements, which together created a narrative reset that the market had not priced. Short-covering in a lightly-held float amplified the magnitude of the single-session move.

—

What is the significance of Digital Turbine’s 2027 guidance in the context of the 2026 macro environment?

In the current 2026 macro environment — characterized by restrictive monetary policy, compressed multiples for unprofitable technology names, and heightened institutional demand for profitability proof points — forward guidance that establishes a revenue growth framework is disproportionately valuable. Prior to this earnings report, Digital Turbine lacked a credible multi-year narrative that institutional analysts could model with confidence. The introduction of FY2027 guidance creates a discount rate anchor and a benchmark against which management credibility will be tested each quarter, effectively unlocking a tier of institutional capital that was previously inaccessible to the stock.

—

What are the key risks investors should monitor following the Digital Turbine Q1 2026 earnings beat?

Three risks warrant close attention: First, the CFO transition — Steve Lasher’s departure introduces execution and financial communications risk at a critical juncture in the turnaround, and the market will scrutinize the incoming CFO’s credibility. Second, gross margin sustainability — at 33.55%, margins remain well below software sector benchmarks, and any deterioration from AI deal implementation costs could reverse the operating leverage narrative. Third, Q2 guidance adherence — with next quarter EPS consensus at $0.09 versus Q1’s $0.16 actual, management has effectively set a lower bar, but consistent delivery against forward estimates is the mechanism through which this turnaround story gains durable institutional sponsorship.

—

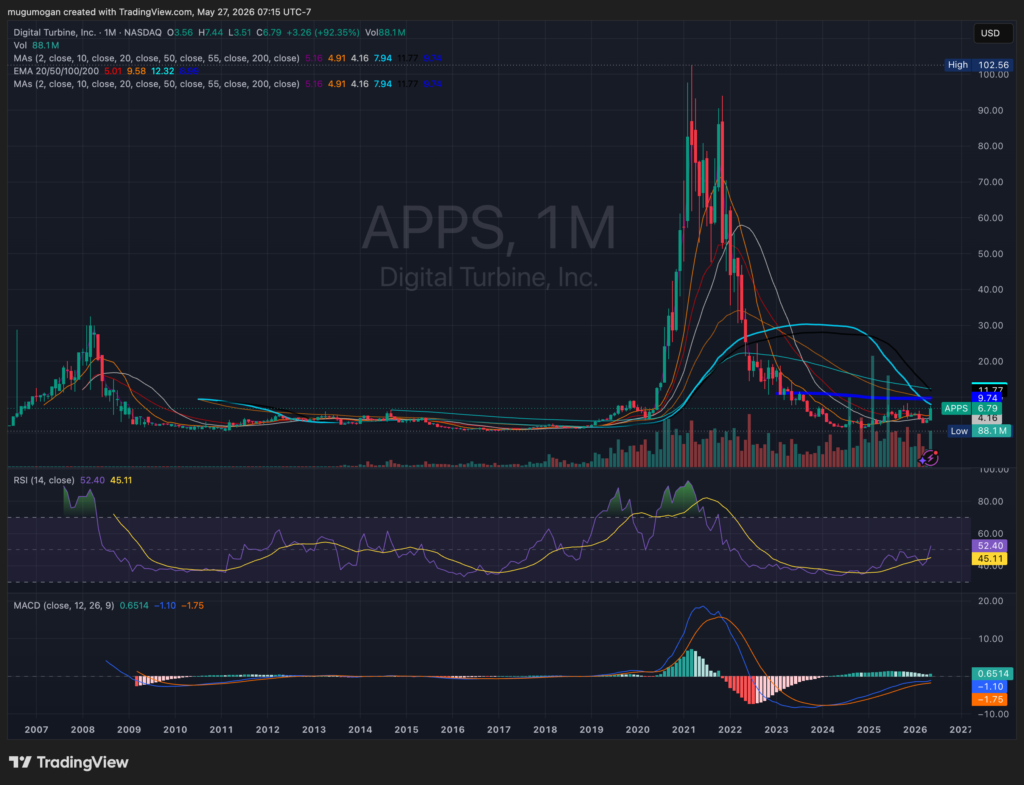

APPS is attempting a major long-term base breakout after a brutal multi-year collapse from the 2021 peak, and the daily chart now shows aggressive momentum expansion with price reclaiming the 50/100/200-day moving averages simultaneously on very heavy volume. The problem is that short-term RSI near 88 is extremely stretched and historically unsustainable, so chasing after a +40% daily candle is statistically poor unless volume continues expanding and the stock can consolidate above the $5.80–6.00 breakout zone instead of immediately failing back below it. On the monthly chart, the real structural test is still ahead near the $9.50–12 region where the declining long-term moving averages and prior breakdown supply sit; if APPS can reclaim that range over coming months, then the entire multi-year downtrend structure starts transitioning from dead-cat behavior into an actual cyclical reversal.