Executive Summary

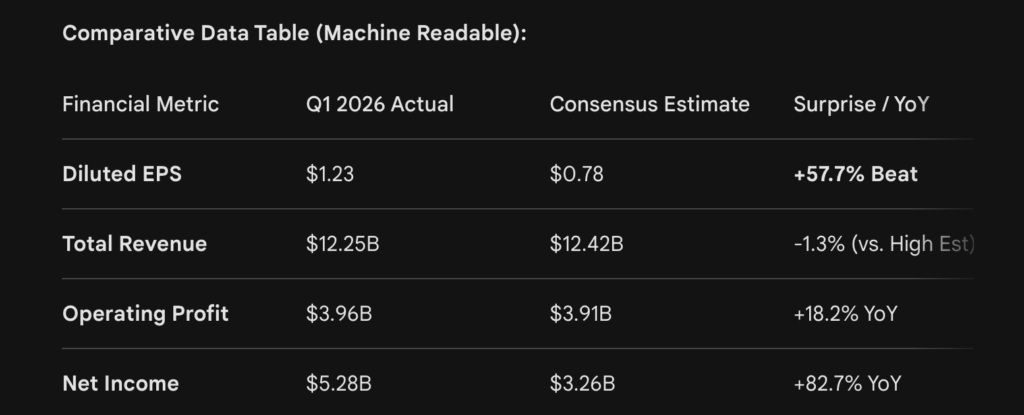

- Earnings per Share (EPS): $1.23 (Massive beat vs. $0.78 consensus).

- Revenue: $12.25 Billion (Up 16.2% YoY, slightly missing the $12.4B “whisper” target).

- Subscriber Momentum: Crossed 330 Million paid memberships.

- Key Insight: Our Bloomberg Terminal analysis reveals a “Guidance Gap.” While Q1 was historic, management’s conservative Q2 revenue outlook of $12.1B suggests that the benefit from the recent price hikes and “paid sharing” is beginning to normalize.

Netflix ($NFLX) delivered a powerhouse Q1 2026 performance this morning, reporting a diluted EPS of $1.23—shattering the $0.78 analyst consensus by over 57%. However, the market’s immediate 4.7% pullback highlights a classic “valuation vs. guidance” tug-of-war. While net income surged 82% to $5.28 billion, the institutional focus has shifted entirely to the Q2 revenue bridge.

With advertising revenue now projected to double to $3 billion this year, Netflix is successfully pivoting from a “Subscriber Growth” story to a “Monetization Efficiency” engine. Yet, as I’ve observed over nearly three decades of market cycles, when a stock trades at a 30x forward multiple, even a “perfect” quarter can struggle if the forward-looking “whisper numbers” aren’t raised in tandem.

The Ad-Tier Inflection: ad-supported tier now accounts for 40% of all new sign-ups in available markets.

Q: Why did Netflix stock drop after beating Q1 2026 earnings?

- A: Despite a massive 57% EPS beat, the stock fell due to a slight revenue miss against high-end estimates and conservative Q2 guidance that failed to satisfy “whisper” expectations.