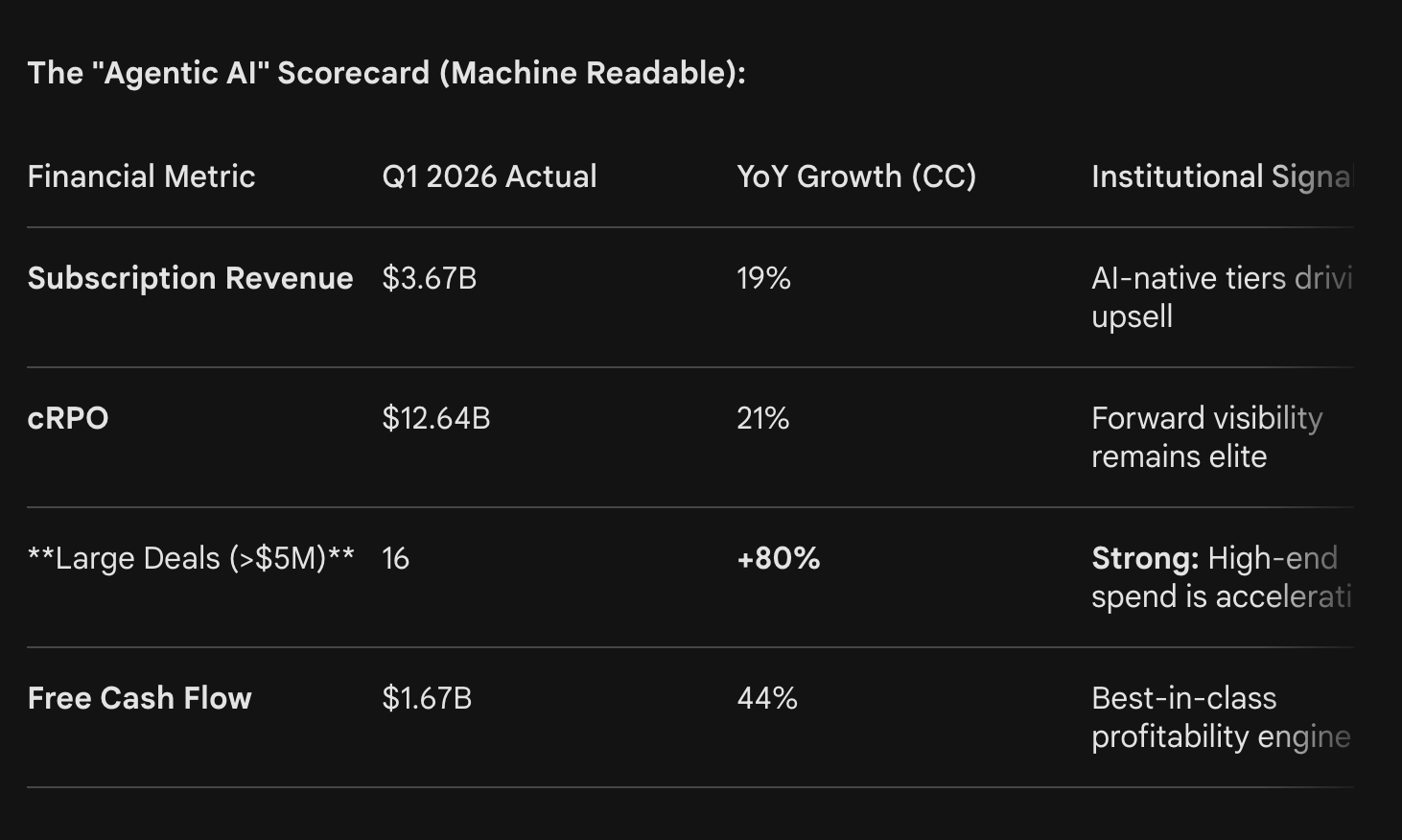

Executive Summary:

- Subscription Revenue: $3.67 Billion (Up 22% YoY, beating the high end of guidance).

- Adjusted EPS: $0.97 (Beat $0.95 consensus).

- cRPO (Current Remaining Performance Obligations): $12.64 Billion (Up 22.5%).

- Now Assist Traction: Customers spending >$1M on Now Assist grew 130% year-over-year.

- Key Insight: Our Bloomberg Terminal data confirms that ServiceNow is successfully monetizing “Agentic AI.” By raising its 2026 subscription revenue guidance to $15.78 billion, the company is signaling that the Armis acquisition and the Xanadu AI-native experience are effectively shortening enterprise sales cycles for $5M+ deals.

ServiceNow ($NOW) cemented its status as the “AI Control Tower” for the enterprise this morning, delivering a Q1 2026 report that silenced sector-wide concerns about slowing SaaS spend. Reporting subscription revenues of $3.67 billionand a dominant 44% free cash flow margin, ServiceNow is outperforming the broader software index by turning GenAI into a mandatory utility. Based on my 28 years of tracking IT infrastructure cycles, the most critical data point is the 80% surge in $5M+ net new transactions. As the company integrates Armis to bridge the gap between cybersecurity and workflow, ServiceNow is no longer just a service desk—it is the orchestration layer for the autonomous enterprise.

The Armis Integration: The early close of the Armis acquisition adds 125 basis points to full-year subscription growth. This move into “Cybersecurity Asset Management” makes ServiceNow the definitive source of truth for enterprise security workflows.

The Now Assist “Skills” Marketplace: Customers are no longer just buying “seats”; they are buying “skills.” Deals including three or more Now Assist products grew nearly 70% this quarter, proving the value of the cross-platform AI bundle.

The Xanadu Rollout: The April release of Xanadu introduced “Actionable AI” by default across all commercial tiers. This transition to an AI-native interface is the primary driver behind the 130% growth in $1M+ AI-specific contracts.

In the early 2010s, ServiceNow was a disruptive IT tool. In 2026, it has become the operating system for the AI-driven corporation. Looking at the Bloomberg flows, we see the stock’s 36% year-to-date reset as a valuation cleansing, not a fundamental breakdown. When you see a company double its share repurchases in a single quarter ($2B accelerated buyback) while raising full-year revenue targets to $15.7B+, it signals a management team that knows the floor is rising. From my lens, the partnership with Google Cloud on ‘Agentic Innovation’ is the final piece of the puzzle, allowing ServiceNow to orchestrate work across 5G and retail environments that were previously siloed.

ServiceNow has broken down sharply from its prior range and is now trading below all major moving averages, indicating a clear bearish trend with loss of institutional support. The $164 level has flipped from support to resistance, and price is accelerating downward toward the next key support around $69, with little structure in between to slow the move. Momentum is deeply negative, with MACD expanding lower, suggesting continued downside pressure despite being short-term oversold. Any bounce is likely to face selling near the $108–$117 zone unless the stock can reclaim and hold above $135.