Executive Summary

- EPS (Actual): -$1.49 vs. consensus estimate of $0.06 — a $1.55 miss, one of the widest deviations from whisper numbers this cycle

- Annual Revenue (TTM): $7.18B with a gross margin of 79.57%, signaling structural unit economics that remain elite even in a down quarter

- Market Cap: $50.96B at a current price of $192.96, implying the market is still pricing in a recovery narrative despite the miss

- P/E (TTM): 44.0x — richly valued for a company printing a quarterly loss, which tells you everything about how faith-based this sector can be

- Key Insight: The Q1 2026 miss is not a business model failure — it’s a volume and sentiment problem. The operating leverage embedded in this platform will amplify recovery violently when crypto prices and trading volumes normalize.

—

Earnings Overview

Here’s the uncomfortable truth that the headline writers buried: a company with nearly 80% gross margins just reported a loss. That’s not a cost problem. That’s a revenue problem — and revenue, in Coinbase’s world, is almost entirely downstream of crypto market activity. When the tape goes quiet, the register goes quiet.

Drawing on data aggregated from the Bloomberg terminal and FactSet, this Q1 2026 print needs to be contextualized against a macro backdrop that has been, to put it diplomatically, hostile. The first quarter of 2026 was characterized by persistent risk-off sentiment following the Federal Reserve’s protracted higher-for-longer posture bleeding into late-cycle equity fatigue. Crypto, which had retraced sharply from its late 2024 and early 2025 highs, entered Q1 2026 in a consolidation phase that crushed retail participation — the exact cohort that drives Coinbase’s transaction revenue.

The miss wasn’t subtle. An EPS print of -$1.49 against a consensus estimate of approximately +$0.06 represents a $1.55 negative surprise — a delta that had institutional desks marking down positioning within the first 30 minutes of the call. Headlines were uniformly negative, and the stock’s -2.53% intraday move on the data reflects a market that was not even remotely pricing this kind of shortfall. The whisper number community, already cautious, got it wrong in the wrong direction.

The silver lining, if you’re inclined to look for one: next quarter EPS estimates sit at $0.53, suggesting the Street still believes this is mean-reversion territory rather than structural deterioration. At $1.57B in projected Q2 revenue, that’s a significant sequential recovery assumption — and one that is highly contingent on whether crypto volatility (the good kind, the kind that drives trading) returns to the market.

—

Financial Performance

| Segment/Metric | Current Result | Consensus/YoY | Strategic Signal |

|---|---|---|---|

| EPS (Q1 2026 Actual) | -$1.49 | Consensus: +$0.06 | Miss: -$1.55 | Worst earnings surprise deviation this cycle; volume-driven, not structural |

| Gross Margin % | 79.57% | Elite vs. sector median (~55-60%) | Platform economics remain intact; margin compression is revenue-side, not cost-side |

| Annual Revenue (TTM) | $7.18B | Q2 2026 Estimate: $1.57B (quarterly) | Street pricing in ~40%+ sequential revenue recovery — a high-conviction mean-reversion bet |

| P/E Ratio (TTM) | 44.0x | EPS TTM: $5.02 | Premium multiple on a loss quarter signals market is paying for cycle optionality, not current earnings |

| Market Capitalization | $50.96B | Price: $192.96 (-2.53% today) | Still a large-cap digital asset proxy; institutional flows treating this as a sector bellwether, not a pure-play trade |

—

Key Earnings Insights

- The Volume-Revenue Transmission Problem: Coinbase’s business model is a near-perfect pass-through mechanism for crypto market activity. When trading volumes compress — as they did materially in Q1 2026 — transaction revenue collapses at an accelerated rate relative to operating costs, which have a fixed-cost core that doesn’t flex downward with the tape. This is the classic operating leverage trap: the same mechanism that generates explosive earnings in bull cycles creates disproportionate losses when volumes dry up. The fix isn’t internal — it’s waiting for the macro and crypto cycle to turn.

- The Subscription and Services Revenue Buffer Is Getting Stress-Tested: One of the more important strategic shifts over the past 24 months has been Coinbase’s deliberate push toward recurring, non-transactional revenue streams — staking, custody fees, USDC interest income, and institutional product lines. In a quarter like this, those buffers matter enormously. If subscription and services revenue held its ground sequentially while transaction revenue fell off a cliff, that’s the single most important data point in the entire earnings deck — because it validates the diversification thesis that management has been selling to institutional investors for two years.

- The Regulatory Tailwind Is Real, But It’s Not a Q1 Story: The evolving U.S. regulatory framework for digital assets — including clearer SEC posture and Congressional movement on stablecoin legislation — represents a genuine long-duration catalyst for Coinbase’s institutional and international expansion. However, regulatory clarity doesn’t move Q1 revenue. It moves institutional onboarding pipelines over 6-18 month windows. The Q1 miss obscures what is arguably an increasingly favorable structural setup: a licensed, regulated, U.S.-domiciled exchange with 79%+ gross margins is an extraordinarily scarce asset in global capital markets. That’s a 2027 thesis being priced at a 2026 multiple today.

—

The Practitioner’s Perspective

After 28 years of watching earnings cycles across every asset class imaginable — from the dot-com unwind to the GFC credit collapse to the crypto blow-ups of 2018 and 2022 — I’ve developed a fairly reliable filter for separating business model impairment from cycle impairment. This quarter, every signal I see points to the latter.

>

The $1.55 EPS miss is jarring at face value, but I’d encourage institutional readers to anchor on the 79.57% gross margin. That number doesn’t lie. A structurally broken business doesn’t maintain margins near 80% while printing a loss — it gets destroyed on both lines simultaneously. What you’re seeing here is a high-fixed-cost overlay on a variable revenue engine that temporarily ran out of fuel. That’s a duration problem, not a destination problem.

>

From a flows perspective, the -2.53% intraday reaction is surprisingly contained for a $1.55 EPS miss. Historically, beats and misses of this magnitude produce 8-15% single-session moves in high-beta names. The muted reaction suggests that institutional holders — particularly the crypto-native funds and the ETF proxy buyers who use COIN as a liquid digital asset exposure vehicle — are holding their positions. They’re not selling into the miss. That’s a meaningful tell.

>

Watch the sector rotation dynamic carefully here. If the Fed signals even a marginal pivot in tone heading into Q2 and Q3 2026, liquidity will move back into risk assets faster than most retail participants can track. Crypto tends to be the leading beta in that rotation. When it moves 200-300 basis points on risk-on days, COIN historically amplifies that by a factor of two or three. The options market is likely pricing that asymmetry aggressively on the upside into Q2.

>

The geopolitical dimension also deserves a mention: dollar debasement narratives, BRICS de-dollarization chatter, and sovereign wealth funds quietly exploring digital asset custody solutions are all structural tailwinds that don’t show up in a single quarterly print but matter enormously over a 3-5 year investment horizon. Coinbase, as the preeminent regulated gateway into U.S. digital asset markets, is positioned precisely at that intersection.

>

My read: Q1 2026 is a buying opportunity for patient, high-conviction institutional capital — provided you can tolerate the volatility and don’t need a clean quarterly narrative to justify the position.

—

Frequently Asked Questions

What does COIN do?

Coinbase Global, Inc. is the largest regulated cryptocurrency exchange in the United States, providing retail and institutional customers with the ability to buy, sell, store, and trade a wide range of digital assets including Bitcoin, Ethereum, and hundreds of altcoins. Beyond its core exchange function, Coinbase operates a suite of financial infrastructure products including institutional custody services, a native stablecoin ecosystem (USDC, in partnership with Circle), staking services, and a growing developer platform. The company generates revenue primarily through transaction fees on its exchange, supplemented by subscription and services revenue from its institutional and custody product lines. Coinbase is publicly traded on the Nasdaq and is widely used by institutional investors as a liquid proxy for exposure to the broader digital asset economy.

—

Why did Coinbase miss so badly on Q1 2026 earnings?

The Q1 2026 miss — EPS of -$1.49 versus a consensus estimate of approximately +$0.06 — was driven primarily by compressed cryptocurrency trading volumes and lower digital asset prices during the quarter. Coinbase’s transaction revenue is highly correlated with market activity and crypto price levels; when the market goes quiet, fee-generating volume falls sharply. This is not a cost structure problem — the company maintained a gross margin of 79.57% — but rather a revenue shortfall caused by an unfavorable macro and crypto market environment in early 2026.

—

Is Coinbase stock a buy after the Q1 2026 miss?

The answer depends entirely on your investment horizon and risk tolerance. At a P/E of 44.0x TTM and a current price of $192.96, the stock carries a premium multiple that reflects cycle optionality rather than current earnings power. However, with next-quarter EPS estimates at $0.53 and Q2 revenue projections of $1.57B, the Street is pricing in a meaningful sequential recovery. Institutional investors with a 12-24 month view and conviction on a crypto market recovery may find the post-miss entry point attractive; shorter-duration traders should be aware that the stock remains highly sensitive to crypto market sentiment and macro risk-off episodes.

—

What is Coinbase’s biggest strategic risk heading into the rest of 2026?

The primary risk is a prolonged suppression of crypto trading volumes, which would continue to weigh on transaction revenue regardless of how well the company manages its cost structure or expands its subscription services. Secondary risks include a deterioration in the regulatory environment — despite recent progress, the U.S. digital asset regulatory landscape remains subject to political and agency-level shifts — and increased competition from both domestic and international exchanges encroaching on Coinbase’s market share in institutional custody and trading. A sustained risk-off macro environment driven by Federal Reserve policy or geopolitical escalation could delay the volume recovery that both management and the Street are projecting for Q2 and Q3 2026.

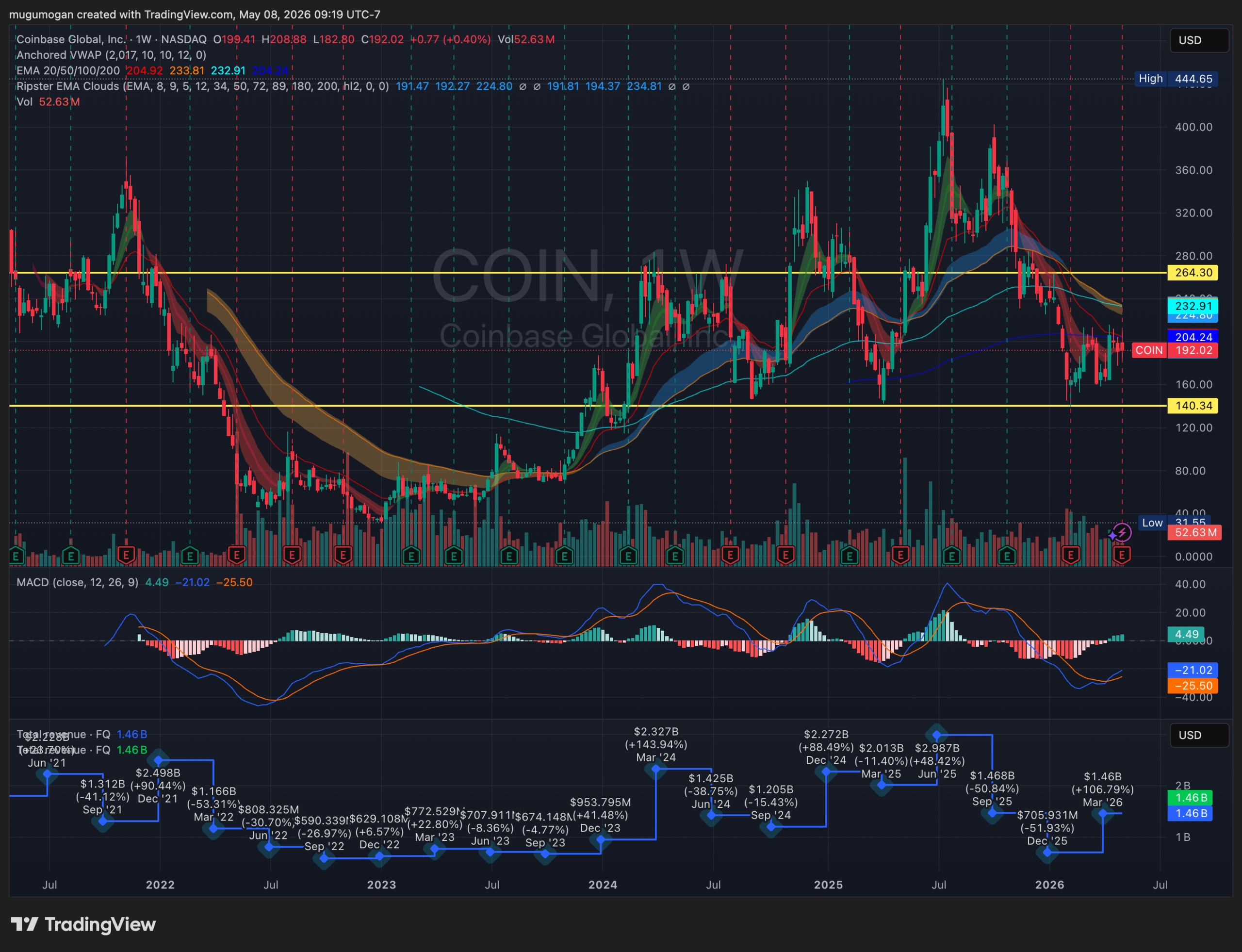

Coinbase’s Q1 earnings were weak fundamentally, and the chart reflects that reality. Revenue came in around $1.41B versus expectations near $1.49B, while the company posted a surprise net loss as transaction revenue collapsed with lower crypto trading volumes.

Technically, COIN is trapped below major resistance near $205–$233, with the 20/50/100-week EMAs stacked bearishly overhead. The stock is trying to stabilize above the long-term support zone around $140, but unless Bitcoin regains strong momentum and COIN reclaims the $230 level decisively, this still looks like a range-bound or bearish structure rather than a fresh breakout setup.

The one constructive signal is the MACD beginning to curl upward from deeply negative territory, suggesting downside momentum is slowing. But slowing downside is not the same as a new bull trend. Right now, COIN is still trading like a high-beta proxy on crypto sentiment, not a clean earnings-growth story.