")

Executive Summary:

Darden Restaurants Inc. is an American multi-brand restaurant operator. It evolved from General Mills Restaurants and has grown to become one of the world’s largest full-service restaurant companies, boasting over 2,100 locations. Darden’s diverse portfolio includes well-known casual dining chains like Olive Garden and LongHorn Steakhouse, alongside fine dining establishments such as The Capital Grille and Eddie V’s. The company emphasizes a strategy focused on delivering consistent food, service, and atmosphere across its various brands.

Darden Restaurants Inc. reported diluted earnings per share (EPS) from continuing operations were $2.74. Adjusted diluted EPS from continuing operations was $2.80, representing a 6.9% increase compared to the same quarter last year. The reported revenue for the quarter was $3.2 billion, which showed a 6.2% increase year-over-year, driven by a 0.7% increase in same-restaurant sales and contributions from the Chuy’s acquisition and new restaurant openings.

Stock Overview:

| Ticker | $DRI | Price | $199.11 | Market Cap | $23.3B |

| 52 Week High | $211.00 | 52 Week Low | $135.87 | Shares outstanding | 117.03M |

Company background:

Darden Restaurants Inc. traces its roots back to 1938 when William “Bill” Darden opened his first restaurant, a 25-seat luncheonette called The Green Frog, in Waycross, Georgia. His commitment to service and welcoming all guests laid the foundation for the company’s future success. In 1968, Darden founded the first Red Lobster restaurant in Lakeland, Florida, which proved to be a pivotal moment. Recognizing its potential, Darden sold Red Lobster to General Mills in 1970, becoming an executive within the conglomerate.

The entity we know today as Darden Restaurants Inc. was officially founded in 1995. This occurred when General Mills spun off its restaurant division into an independent publicly traded company, retaining the name of its visionary founder, Bill Darden. While the initial funding came from General Mills’ backing of Red Lobster, it raised capital through stock offerings and generated revenue through its extensive restaurant operations.

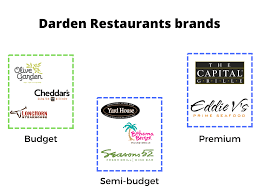

Darden Restaurants boasts a diverse portfolio of well-known full-service restaurant brands, catering to various dining preferences and price points. These brands can be broadly categorized into casual dining and fine dining. The casual dining segment includes Olive Garden, known for its Italian-American cuisine and breadsticks; LongHorn Steakhouse, specializing in grilled steaks and American fare; Cheddar’s Scratch Kitchen, offering made-from-scratch comfort food; Yard House, a sports bar with a wide selection of beers and American cuisine; and Bahama Breeze, featuring Caribbean-inspired dishes and cocktails. The fine dining segment comprises The Capital Grille, an upscale steakhouse and wine bar; Eddie V’s Prime Seafood, offering premium seafood and live jazz music; and Seasons 52, a fresh grill and wine bar with a seasonally inspired menu.

In the competitive full-service restaurant industry, Darden Restaurants faces competition from a variety of national and regional chains. Key competitors include companies with a strong presence in casual dining, such as Chipotle Mexican Grill (CMG), Yum! Brands (YUM) (parent company of KFC, Pizza Hut, and Taco Bell), Domino’s Pizza (DPZ), Texas Roadhouse (TXRH), Brinker International (EAT) (parent company of Chili’s and Maggiano’s), Wendy’s (WEN), and The Cheesecake Factory (CAKE). In the fine dining segment, competitors include other upscale steakhouse and seafood chains.

Darden Restaurants Inc. is headquartered in Orlando, Florida, in the United States. The company oversees its numerous brands and thousands of employees from this main office, strategically positioned in a region known for its tourism and hospitality industry.

Recent Earnings:

Darden Restaurants Inc. reported total revenue of $3.2 billion, representing a 6.2% increase compared to the $2.97 billion reported in the same quarter of the previous year. This growth was primarily attributed to a 0.7% increase in same-restaurant sales and the contribution from the acquisition of 103 Chuy’s restaurants and the opening of 40 net new restaurants. The blended same-restaurant sales increase of 0.7% was driven by varying performances across Darden’s brands, with LongHorn Steakhouse showing a positive growth of 2.6%, while Fine Dining experienced a slight decrease of 0.8%. Olive Garden reported a modest increase of 0.6%, and the Other Business segment, which now includes Chuy’s, saw a decrease of 0.4% on a same-restaurant sales basis.

Darden reported diluted net earnings per share (EPS) from continuing operations of $2.74. Excluding certain transaction and integration costs related to the Chuy’s acquisition, the adjusted diluted EPS from continuing operations was $2.80, which represents a 6.9% increase compared to the adjusted EPS of $2.62 in the third quarter of fiscal year 2024. While the reported revenue of $3.2 billion was slightly below the analysts’ consensus estimate of $3.22 billion, the adjusted EPS of $2.80 was also marginally below the expected $2.81.

Darden highlighted that all its operating segments – Olive Garden, LongHorn Steakhouse, Fine Dining, and Other Business – experienced growth in total sales and segment profit margin during the third quarter. The company also noted strong sales performance during the holiday season and Valentine’s Day, underscoring the strength of its brand portfolio and guest loyalty. Darden continued its capital allocation strategy by repurchasing approximately 0.3 million shares of its common stock for a total of $53 million during the quarter. As of the end of the third quarter, the company had $548 million remaining under its current $1 billion repurchase authorization. Darden’s Board of Directors declared a quarterly cash dividend of $1.40 per share, payable on May 1, 2025, to shareholders of record as of April 10, 2025.

The company anticipates total sales of approximately $12.1 billion for the full fiscal year. They project same-restaurant sales growth of approximately 1.5%. Darden plans to open 50 to 55 new restaurants and expects total capital spending of around $650 million. The company also anticipates a total inflation rate of approximately 2.5% and an effective tax rate of about 12.5%. The weighted average diluted shares outstanding are expected to be approximately 118.3 million. Darden projects adjusted diluted net earnings per share from continuing operations to be in the range of $9.45 to $9.52, excluding the aforementioned Chuy’s transaction and integration costs.

The Market, Industry, and Competitors:

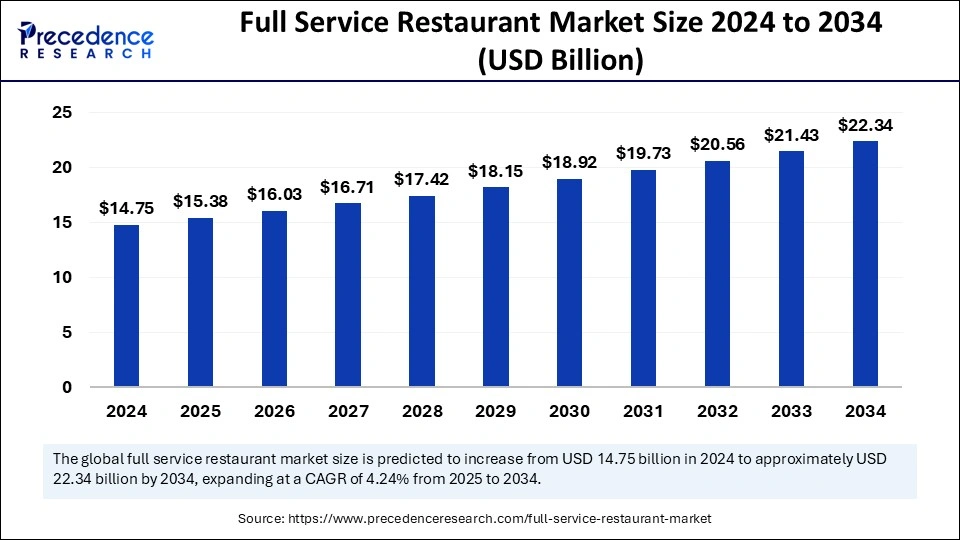

Darden Restaurants Inc. operates within the expansive and competitive full-service restaurant market. This market encompasses a wide array of dining establishments, from casual dining chains like Olive Garden and LongHorn Steakhouse to fine dining experiences such as The Capital Grille and Eddie V’s. The full-service segment distinguishes itself from quick-service restaurants (QSRs) by offering table service and a more comprehensive menu. Factors influencing this market include consumer disposable income, lifestyle trends, culinary preferences, and the overall economic climate. The industry is also increasingly shaped by technological advancements, including online ordering, delivery services, and digital customer engagement, as well as evolving consumer demands for healthier and more sustainable dining options.

A compound annual growth rate (CAGR) in the range of 2.8% to 6.39% between 2024/2025 and 2030. This growth is expected to be driven by factors such as increasing urbanization, rising disposable incomes in developing economies, a growing preference for convenience and dining out, and the ongoing integration of technology to enhance the dining experience. The North American market, where Darden has a significant presence, is also anticipated to see steady growth, with one report suggesting a CAGR of 4.42% for the full-service restaurant market in the region between 2025 and 2034.

The company’s diverse brand portfolio positions it well to cater to different segments of the full-service market. Growth expectations for Darden will likely be influenced by its ability to adapt to changing consumer preferences, effectively manage operational costs in the face of inflation, leverage technology to improve efficiency and customer engagement, and strategically expand its footprint through new restaurant openings and potential acquisitions. The projected overall growth of the full-service restaurant market suggests a favorable environment for Darden to continue expanding its revenue and profitability through the end of the decade.

Unique differentiation:

Darden Restaurants Inc. operates in both the casual dining and fine dining segments of the restaurant industry, leading to a diverse set of competitors. In the casual dining space, Darden’s Olive Garden, LongHorn Steakhouse, Cheddar’s Scratch Kitchen, Yard House, and Bahama Breeze brands face significant competition from large national chains such as Chipotle Mexican Grill (CMG), Yum! Brands (YUM) (parent company of KFC, Pizza Hut, and Taco Bell), Domino’s Pizza (DPZ), Texas Roadhouse (TXRH), Brinker International (EAT) (parent company of Chili’s and Maggiano’s), Wendy’s (WEN), The Cheesecake Factory (CAKE), Cracker Barrel Old Country Store (CBRL), and BJ’s Restaurants (BJRI). These competitors vie for a similar customer base seeking a relaxed dining experience with a focus on value and a varied menu. The competitive landscape in casual dining is intense, with companies focusing on menu innovation, promotional offers, and maintaining a strong brand identity to attract and retain customers.

Darden’s fine dining brands, The Capital Grille and Eddie V’s Prime Seafood, operate in a more upscale segment with a different set of key competitors. These brands compete with other high-end steakhouse and seafood chains known for their premium quality food, extensive wine lists, sophisticated ambiance, and exceptional service. Competitors in this space often include establishments like Ruth’s Hospitality Group (acquired by Darden in 2023 but still a distinct concept to consider in the broader market), Morton’s The Steakhouse, Del Frisco’s Double Eagle Steakhouse, and various other regional and national fine dining groups. The focus in this segment is on creating a memorable and luxurious dining experience, often with higher price points and a more discerning clientele. Competition in fine dining centers on the quality of ingredients, the expertise of the chefs, the level of service, and the overall atmosphere of the restaurant.

The restaurant industry as a whole faces competition from various dining alternatives, including fast-casual restaurants that bridge the gap between quick service and casual dining, as well as the increasing popularity of meal delivery services and at-home cooking trends. Companies like Panera Bread, Sweetgreen, and Five Guys represent the fast-casual segment, offering a different value proposition to consumers. The ability of Darden Restaurants to effectively differentiate its brands within their respective segments and adapt to broader industry trends will be crucial for maintaining its competitive edge.

Darden Restaurants Inc. distinguishes itself from competitors through a multifaceted approach built on its significant scale and diverse brand portfolio. Unlike many restaurant companies that focus on a single concept or a narrower range, Darden operates a collection of well-established and distinct brands across different dining segments, including casual (Olive Garden, LongHorn Steakhouse, Cheddar’s Scratch Kitchen, Yard House, Bahama Breeze) and fine dining (The Capital Grille, Eddie V’s, Seasons 52, Ruth’s Chris Steak House, Chuy’s). This diversification allows Darden to cater to a broader range of consumer preferences, occasions, and price points, mitigating risks associated with the performance of a single brand or market segment. The sheer size of the organization provides substantial economies of scale in areas like supply chain management, distribution, and marketing, leading to cost advantages that individual brands might not achieve on their own.

Another key differentiator is Darden’s deep understanding and utilization of data and insights. With its vast network of restaurants serving millions of guests annually, Darden accumulates a wealth of data on customer preferences, dining trends, and operational efficiencies. The company leverages this data to inform strategic decisions across its brands, including menu innovation, pricing strategies, marketing campaigns, and operational improvements. This data-driven approach enables Darden to better understand and meet guest expectations, identify opportunities for growth, and make more impactful decisions compared to competitors with less extensive data resources.

Darden emphasizes a “Back-to-Basics” operating philosophy that focuses relentlessly on strong in-restaurant execution. This involves a deep commitment to culinary innovation and consistent food quality, attentive and personalized service, and creating inviting and engaging atmospheres within each distinct brand. This focus on the fundamental aspects of the dining experience aims to build guest loyalty and ensure consistent positive experiences across all its locations. Coupled with a results-oriented culture that values its employees and invests in their success, Darden strives to create a competitive advantage through its people and its unwavering commitment to the core elements of hospitality.

Management & Employees:

Rick Cardenas serves as the President and Chief Executive Officer. He has been with Darden for many years, previously holding roles such as Chief Operating Officer and Chief Financial Officer. His long tenure and deep understanding of the company’s operations and strategy are crucial for guiding Darden’s overall direction and growth.

Raj Vennam is the Senior Vice President and Chief Financial Officer. He is responsible for overseeing the company’s financial strategy, reporting, and investor relations. His expertise in finance and analytics plays a vital role in Darden’s financial health and strategic decision-making.

Dan Kiernan serves as the President of Olive Garden, the company’s largest brand.

Laura Williamson holds the position of President of LongHorn Steakhouse.

Financials:

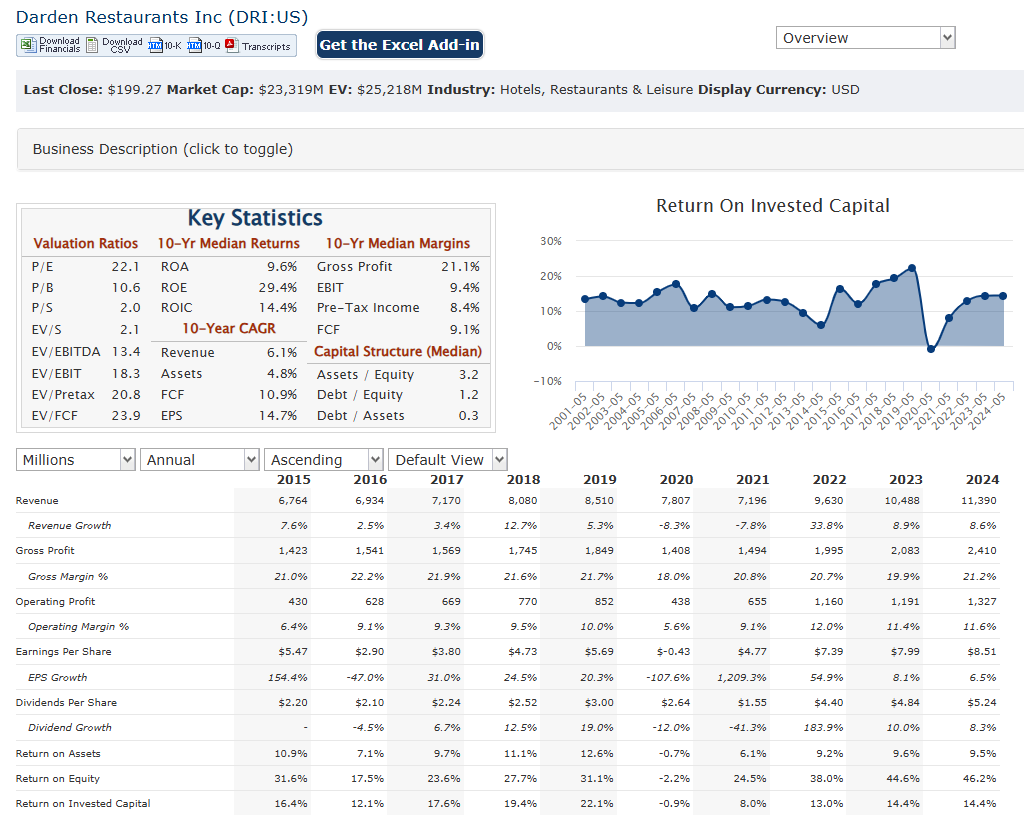

Darden Restaurants Inc. has demonstrated consistent financial growth, driven by its diversified portfolio of brands such as Olive Garden and LongHorn Steakhouse. From fiscal 2020 to fiscal 2024, Darden’s revenue grew at a compound annual growth rate (CAGR) of approximately 3.5%, reaching $11.39 billion in fiscal 2024, up from $10.49 billion in fiscal 2023. This growth was supported by new restaurant openings, strategic acquisitions (such as Chuy’s in 2024), and modest same-restaurant sales increases across key brands, though some segments like Fine Dining faced periodic declines.

Earnings growth has been steady but faced challenges from rising costs and economic headwinds. Adjusted diluted earnings per share (EPS) increased by a CAGR of about 5% over the last five years, reflecting operational efficiency and disciplined cost management. In fiscal 2025’s third quarter, adjusted EPS grew 6.9% year-over-year to $2.80, highlighting resilience despite inflationary pressures. However, occasional dips in same-restaurant sales, such as a 1.1% decline in the first quarter of fiscal 2025, underscore ongoing challenges in maintaining consistent profitability across all segments.

Darden’s balance sheet reflects a strong but leveraged position. As of late 2024, the company held $198.67 million in cash against $7.40 billion in total debt, translating to a high debt-to-equity ratio of approximately 391%. Despite this leverage, Darden has maintained robust returns on equity (50.93%) and assets (7.06%), supported by strong free cash flow generation of $700 million annually. The company has also actively returned capital to shareholders through dividends and share repurchases, with a five-year average dividend yield of 2.83%.

Overall, Darden’s financial performance over the past five years reflects its ability to navigate economic challenges while delivering steady growth and shareholder value. Strategic acquisitions and operational improvements have bolstered its revenue and earnings trajectory, although balancing debt levels remains a priority for sustained long-term growth.

Technical Analysis:

The stock is in a stage 2 bullish markup on the monthly chart, and consolidation stage 3 neutral on the weekly chart. The daily chart is in a consolidation stage 3 as well and if the stock breaks over the $202 zone, it should turn higher to $212 area, but is likely to head lower to support at $190

Bull Case:

Diversified portfolio of well-established brands: With concepts spanning various dining occasions and price points, from the casual appeal of Olive Garden and LongHorn Steakhouse to the upscale experience of The Capital Grille and Eddie V’s, Darden can capture a wider customer base and is more resilient to shifts in consumer preferences within a specific dining segment. The recent acquisitions of Ruth’s Chris Steak House and Chuy’s further enhance this diversification and offer opportunities for synergies and expanded market reach. This multi-brand strategy helps mitigate risks associated with any single brand underperforming.

Scale and operational efficiency: As one of the largest full-service restaurant companies, Darden benefits from significant economies of scale in its supply chain, purchasing power, and distribution networks. This allows for better cost management and potentially higher profit margins compared to smaller competitors. The company’s consistent focus on in-restaurant execution and leveraging data analytics to optimize operations and understand customer behavior further supports efficient and profitable growth.

Bear Case:

Economic sensitivity and consumer discretionary spending. As a full-service restaurant company, Darden’s brands are vulnerable to economic downturns and shifts in consumer behavior. During periods of economic uncertainty or recession, consumers may reduce discretionary spending on dining out, opting for more affordable options like quick-service restaurants or cooking at home. This could lead to decreased traffic and slower sales growth across Darden’s portfolio, impacting revenue and profitability. Rising inflation, particularly in food and labor costs, could further pressure margins if Darden is unable to fully pass these costs on to consumers without negatively affecting demand.

Competitive pressures and evolving consumer preferences. The restaurant industry is highly competitive, with numerous national, regional, and local players vying for market share. Darden faces competition not only from other full-service chains but also from the growing fast-casual segment and the increasing popularity of meal delivery services. Changing consumer tastes and preferences, including a growing demand for healthier options and more diverse cuisines, could also pose a challenge if Darden’s brands fail to adapt effectively. Furthermore, negative perceptions or trends associated with any of Darden’s major brands could significantly impact overall performance.

Integration risks associated with acquisitions represent a potential concern. While Darden’s recent acquisitions of Ruth’s Chris Steak House and Chuy’s offer growth opportunities, they also come with inherent integration challenges. These include potential difficulties in combining operations, managing different cultures, and achieving anticipated synergies. If these integrations are not executed smoothly, they could lead to unexpected costs and a drag on overall financial performance. Moreover, any misjudgment in the acquisition strategy or overpayment for these businesses could negatively impact shareholder returns.