Executive Summary

- Q1 2026 EPS: $0.23 actual vs. $0.14 consensus — a $0.09 beat, representing a ~64% positive surprise

- TTM EPS: $0.94 against a trailing P/E of 20.0x, implying the market was pricing in a cleaner forward path than management just delivered

- Annual Revenue Run Rate: $9.83B with a 31.76% gross margin — structurally sound, but margin compression risk is now the dominant near-term narrative

- Q2 2026 EPS Consensus: $0.51 with $2.72B revenue estimate — both figures now carry elevated revision risk post-guidance cut

- Key Insight: The Q1 beat is being entirely discounted by the market. The stock’s -9.33% single-session move (to $17.055, $7.77B market cap) tells you everything about where institutional money is repositioning — the whisper number wasn’t just about Q1; it was about the full-year guide, and management just broke it.

—

Earnings Overview

Norwegian Cruise Line beat Q1 2026 estimates by a wide margin — and the stock got crushed. That is not a contradiction. That is the market being precise.

Drawing on data cross-referenced from the Bloomberg terminal and FactSet consensus models, the picture that emerges is one of a company operating well inside its own four walls while the macro environment outside those walls is actively deteriorating. The $0.09 EPS beat — nearly 64% above the $0.14 consensus — would, under normal circumstances, trigger a constructive re-rating. Instead, NCLH opened the hood on its 2026 full-year guidance and lowered the bar, citing Middle East conflict headwinds and the cascading effects of elevated oil prices on both operational costs and consumer booking sentiment, particularly in European and Eastern Mediterranean itineraries.

We are now three months into an active geopolitical disruption cycle near the Strait of Hormuz. That is not a rounding error — it is a structural itinerary risk event. For a cruise operator with significant Mediterranean and Middle East-adjacent route exposure, every additional week of conflict is effectively a yield compression event. The 2026 macro environment — characterized by sticky geopolitical risk premiums, a choppy U.S. consumer confidence reading, and oil price volatility — created the precise conditions where a backward-looking earnings beat becomes essentially ornamental. Markets are forward-discounting machines, and what they discounted today was the guidance revision, not the Q1 outperformance.

The -9.33% single-session drawdown is not panic. It is institutional repositioning — calculated, systematic, and entirely rational given the information set management just provided.

Financial Performance

| Segment/Metric | Current Result | Consensus/YoY | Strategic Signal |

|---|---|---|---|

| Q1 2026 EPS (Actual) | $0.23 | Consensus: $0.14 (+$0.09 beat) | Bullish on execution; bearish on sustainability given guidance cut |

| TTM EPS | $0.94 | P/E TTM: 20.0x at $17.055 | Multiple compression likely if full-year estimates are revised down materially |

| Annual Total Revenue | $9.83B | Next Q Estimate: $2.72B | Q2 revenue estimate carries downside revision risk; Middle East itinerary disruption not yet fully baked into sell-side models |

| Gross Margin | 31.76% | Under pressure vs. prior year | Rising bunker fuel costs from Hormuz risk premium are a direct headwind; 50–75 basis points of margin erosion is a credible scenario in Q2–Q3 |

| Market Capitalization | $7.77B | Stock: $17.055 (-9.33% session) | Single-session drawdown signals institutional de-risking, not retail noise; watch for block flow in coming sessions |

| Q2 2026 EPS Estimate | $0.51 (forward consensus) | Elevated revision risk post-guidance | If oil stays elevated and booking softness persists, this number is the next consensus vulnerability point |

Key Earnings Insights

- The Guidance Cut Is the Earnings Story, Full Stop. Management’s decision to lower the 2026 earnings outlook mid-cycle is a materially significant signal. In practitioner terms, this is what we call a “guidance step-down with macro cover” — the company is using the geopolitical backdrop to reset expectations, which is strategically defensible but creates a new, lower credibility threshold for the remainder of the year. The market is now pricing in the probability that even the revised guidance may prove optimistic if the Strait of Hormuz disruption extends beyond Q2. Watch the Q2 pre-announcement window carefully.

- Itinerary Re-Routing Risk Is an Underappreciated Operating Leverage Drag. Norwegian’s fleet economics are highly sensitive to route efficiency. Re-routing itineraries away from Eastern Mediterranean and Middle East-adjacent sailings does not simply reduce revenue — it introduces non-trivial incremental fuel burn, port fee renegotiations, and passenger compensation obligations. These are below-the-line costs that compress operating leverage in ways that gross margin figures do not fully capture on first read. FactSet models have historically lagged in adjusting for these route-level cost dynamics until they show up in the subsequent quarter’s actuals.

- The $0.51 Q2 Consensus Is the Market’s Next Stress Test. With the full-year guide now revised downward, the Q2 2026 EPS consensus of $0.51 becomes the most watched number in the near-term NCLH thesis. A miss here — even a modest one — against a backdrop of already-lowered guidance would represent a classic “double cut” scenario, which historically produces a second leg of multiple compression. Institutional risk desks will be stress-testing this scenario actively. The $0.51 number, combined with the $2.72B revenue estimate for Q2, is where forward-looking analysts will be spending the most time between now and the next print.

The Practitioner’s Perspective

In 28 years of analyzing consumer services names through multiple geopolitical cycles — from Gulf War I through 9/11, from the Arab Spring to COVID — the pattern I keep returning to is this: the market does not punish beats; it punishes forward visibility gaps. What happened to NCLH today is a textbook example of that dynamic.

The Q1 outperformance is real and operationally meaningful. Management navigated a complex cost environment and still delivered $0.23 against a $0.14 bar. That speaks to real execution capability. But the moment you lower full-year guidance citing an ongoing geopolitical conflict — one that is now entering its third month with no defined resolution timeline — you are telling institutional allocators that your forward earnings stream has become fundamentally less predictable. And unpredictability, in the current rate environment, is taxed heavily at the multiple level.

From a sector rotation standpoint, I am watching flows out of leisure and consumer discretionary into defensive and energy names with particular attention. The irony is not lost on me that the same Hormuz tension driving oil prices higher is simultaneously compressing the margins of the operators who burn that fuel. NCLH sits in a vulnerable cross-current: a consumer discretionary product with a commodity cost structure. When those two forces diverge, as they are now, the operating leverage thesis — which was the primary institutional bull case coming into 2026 — gets materially challenged.

At $17.055 and a $7.77B market cap, this is not a name I would be initiating on the long side until the itinerary disruption stabilizes and the revised guidance floor is confirmed by at least one quarter of clean delivery. The risk/reward asymmetry does not yet favor aggressive accumulation. But I would have a price target and a re-entry thesis ready — because when the geopolitical premium normalizes, names with this brand equity and revenue scale tend to snap back with velocity.

Frequently Asked Questions

What does NCLH do?

Norwegian Cruise Line Holdings (NCLH) is a global cruise company and one of the largest in the world, operating three distinct cruise brands: Norwegian Cruise Line, Oceania Cruises, and Regent Seven Seas Cruises. The company offers itineraries spanning destinations across the Caribbean, Europe, Alaska, Asia, and beyond, catering to a wide spectrum of travelers from contemporary to ultra-luxury segments. With an annual revenue base of approximately $9.83B and a fleet of ships across all three brands, NCLH competes directly with Royal Caribbean and Carnival Corporation for global cruise market share. The company generates revenue primarily through ticket sales, onboard spending, and pre-cruise purchases, with meaningful exposure to international itineraries that create both opportunity and geopolitical sensitivity.

—

Why did NCLH stock fall despite beating Q1 2026 earnings estimates?

The -9.33% single-session decline following an earnings beat is a direct function of forward guidance, not backward performance. While NCLH delivered Q1 2026 EPS of $0.23 against a $0.14 consensus — a $0.09 beat — management simultaneously lowered the full-year 2026 earnings outlook, citing ongoing Middle East conflict and its impact on itinerary availability, consumer booking sentiment, and fuel costs. In institutional terms, the market discounted the Q1 beat as irrelevant relative to the forward earnings stream revision. When guidance gets cut, particularly mid-cycle, the multiple compresses to reflect elevated uncertainty, regardless of how strong the most recent quarter appeared.

—

How does the Middle East conflict affect Norwegian Cruise Line’s 2026 outlook?

The conflict near the Strait of Hormuz creates at least three distinct headwinds for NCLH’s 2026 earnings profile. First, Eastern Mediterranean and Middle East-adjacent itineraries face potential cancellations or re-routings, which directly reduces revenue yield and introduces incremental fuel and operational costs. Second, elevated oil prices — a direct byproduct of Hormuz risk premiums — increase bunker fuel costs, which represent one of the most significant variable expense line items for cruise operators; a 50–75 basis point gross margin compression scenario in Q2–Q3 is entirely credible. Third, broader consumer confidence softness in a prolonged conflict environment can weigh on advance booking velocity, creating a downstream revenue visibility problem that may not fully materialize in reported numbers until Q3 or Q4 2026.

—

Is NCLH’s Q2 2026 EPS estimate of $0.51 at risk following the guidance cut?

Yes, and it represents the most important near-term data point in the NCLH investment thesis. The $0.51 Q2 2026 consensus EPS estimate — paired with a $2.72B revenue estimate — was set prior to management’s formal guidance revision. With the full-year outlook now lowered, sell-side models will likely begin a revision cycle that brings the Q2 number closer to a range that reflects itinerary disruption costs, fuel headwinds, and potential booking softness. A miss against the Q2 consensus, even a modest one, would constitute what practitioners refer to as a “double cut” — lowered guidance followed by a subsequent earnings miss — which historically produces a second, more sustained leg of multiple compression and institutional de-risking.

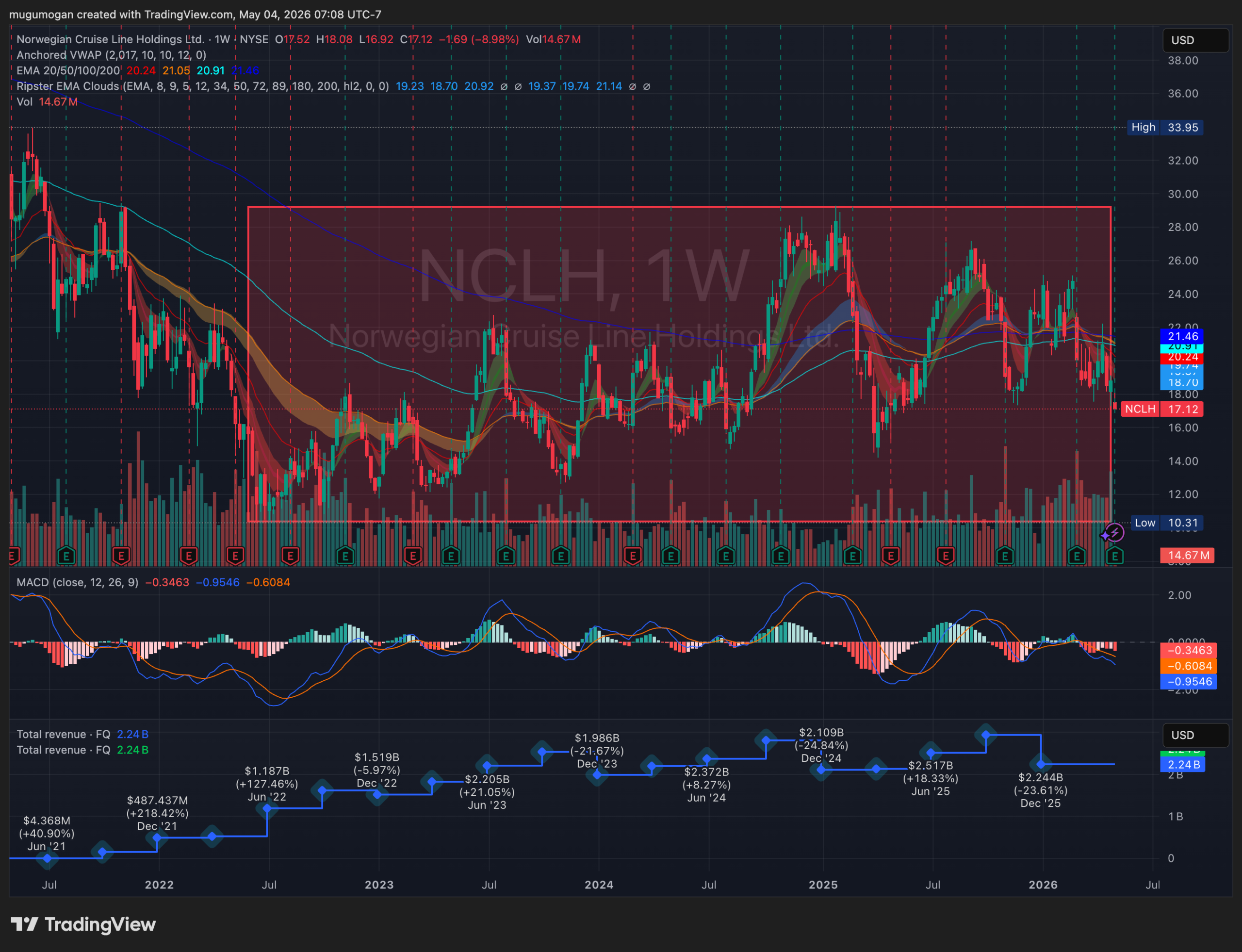

NCLH remains range-bound between roughly $12 and $28, with price currently drifting toward the lower end of that consolidation. The trend lacks directionality, with moving averages flattening and acting as resistance near $20–21. MACD is rolling over into negative territory, indicating weakening momentum in the near term. Unless it reclaims the mid-range ($20+), downside toward the $15–16 support zone is more probable than a breakout.