")

Executive Summary:

Expedia Group Inc. is a leading global travel technology company that provides a wide range of travel services, including booking flights, hotels, car rentals, and vacation packages. Operating a vast network of online travel brands, the company leverages its technology platform to connect travelers with a diverse range of travel providers worldwide. Expedia Group aims to simplify the travel planning process for individuals and businesses.

Expedia Group Inc. reported a GAAP EPS of $2.80, marking a 10% increase from the previous year, while the adjusted EPS rose 21% to $3.51. Revenue for the quarter reached $3.6 billion, reflecting a 6% year-over-year growth and surpassing analyst estimates of $3.53 billion.

Stock Overview:

| Ticker | $EXPE | Price | $152.09 | Market Cap | $19.80B |

| 52 Week High | $160.05 | 52 Week Low | $92.48 | Shares outstanding | 124.66M |

Company background:

Expedia Group Inc., a leading global travel technology company, was founded in 1999 by Jake Jaber, Rich Barton, and Jeffrey Katz. The company initially started as a small online travel agency focused on booking flights. With its innovative approach and strategic acquisitions, Expedia Group has grown into a dominant player in the travel industry.

The company has received significant funding throughout its history, with major investors including IAC/InterActiveCorp and Expedia itself. This funding has enabled Expedia Group to expand its operations, develop new technologies, and acquire other travel companies. Some of the notable acquisitions include Travelocity, Hotwire, and Orbitz.

Expedia Group offers a wide range of travel products and services, catering to both leisure and business travelers. Its platform allows users to book flights, hotels, car rentals, vacation packages, and activities worldwide. The company also provides travel-related tools and information, such as destination guides, reviews, and travel inspiration.

Key competitors of Expedia Group include Booking Holdings (formerly Priceline Group), TripAdvisor, and Ctrip. These companies operate in similar markets and offer competing travel services. Expedia Group differentiates itself through its extensive network of travel partners, user-friendly interface, and personalized recommendations. The headquarters of Expedia Group Inc. is located in Bellevue, Washington, USA.

Recent Earnings:

Expedia Group Inc. reported revenue of $3.9 billion, which represents a 7% increase compared to the same quarter last year. This growth was driven by robust demand across its travel services, particularly in lodging and vacation rentals, as consumers continue to prioritize travel experiences post-pandemic. Analysts had anticipated revenue of approximately $3.75 billion, indicating that Expedia outperformed market expectations by a notable margin.

Earnings per share (EPS), Expedia reported a GAAP EPS of $2.95, reflecting a 15% year-over-year increase. The adjusted EPS came in at $3.67, exceeding analyst forecasts of $3.50. This strong performance in EPS highlights the company’s effective cost management strategies and operational efficiencies, which have allowed it to capitalize on the increasing travel demand while maintaining profitability.

Operational metrics also with gross bookings rising by 8% to reach $29.5 billion for the quarter. The company experienced significant growth in international bookings, which surged by 12%, underscoring a rebound in global travel. Expedia’s active customer base expanded, with a notable increase in repeat bookings, indicating strong customer loyalty and satisfaction.

Expedia provided optimistic forward guidance for Q4 2024, projecting revenue between $4 billion and $4.2 billion, driven by continued strength in travel demand during the holiday season. The company expects EPS to range from $3.10 to $3.30, reflecting confidence in its operational strategies and market positioning.

The Market, Industry, and Competitors:

Expedia Group operates in the highly competitive online travel market, which is characterized by rapid technological advancements, changing consumer preferences, and intense competition from both established players and new entrants. The company competes with major players like Booking Holdings (formerly Priceline Group), TripAdvisor, and Ctrip, as well as a variety of regional and niche travel agencies.

The online travel market is expected to experience growth, driven by factors such as rising disposable incomes, increasing urbanization, and the growing popularity of online travel booking platforms. The global online travel market is projected to reach a value of USD 1,036.7 billion by 2030, growing at a CAGR of 8.9% during the period 2023-2030.

Unique differentiation:

Booking Holdings (formerly Priceline Group): Booking Holdings is one of the largest online travel companies in the world, operating a portfolio of brands including Booking.com, Priceline, Agoda, Kayak, and Rentalcars.com. The company offers a wide range of travel services, including hotel bookings, flight reservations, car rentals, and vacation packages.

TripAdvisor: TripAdvisor is a leading travel website that provides reviews and information on hotels, restaurants, attractions, and activities. The company also offers booking services for hotels and flights. TripAdvisor’s extensive user-generated content and strong brand recognition make it a formidable competitor.

MakeMyTrip: MakeMyTrip is a leading Indian online travel agency that offers a wide range of travel services, including hotel bookings, flight reservations, car rentals, and vacation packages. The company’s strong presence in the Indian market and its growing international operations make it a significant competitor.

Extensive Network: Expedia Group has a vast network of travel partners, including airlines, hotels, car rental companies, and activity providers, offering travelers a wide range of options to choose from.

Personalized Recommendations: The company leverages its data and technology to provide personalized recommendations to travelers, based on their preferences and past booking history.

Loyalty Programs: Expedia Group offers loyalty programs that reward frequent travelers with points and benefits, encouraging customer loyalty and repeat business.

Management & Employees:

Peter Kern: Chief Executive Officer

Emily Koblenz: Chief Marketing Officer

John Kim: Chief Product Officer

Alison Taylor: President, Expedia for Business

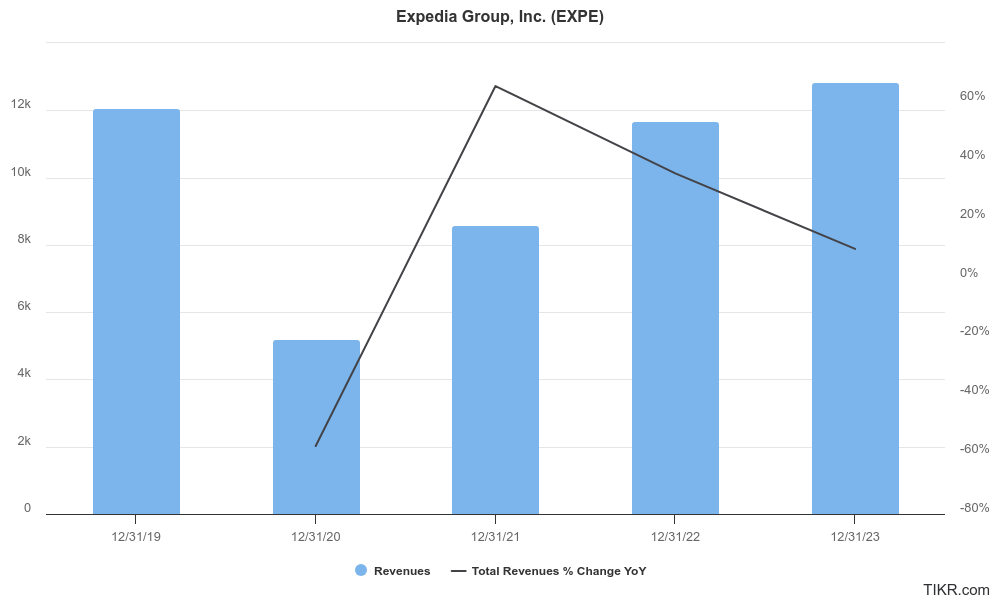

Financials:

Expedia Group Inc. has reported revenue of approximately $12.07 billion, which declined sharply to $5.2 billion in 2020 due to travel restrictions and decreased consumer demand. However, as travel resumed, Expedia’s revenue rebounded to $8.6 billion in 2021, and further increased to $11.67 billion in 2022, culminating in $12.84 billion for 2023.

The compound annual growth rate (CAGR) for revenue over these five years stands at around 4%, highlighting a recovery trajectory post-pandemic. Earnings per share (EPS) have also shown a volatile trend during this timeframe. In 2019, EPS was reported at $3.84, which plummeted to a loss of -$19.29 in 2020 as the company faced unprecedented challenges. A modest recovery was seen in 2021 with an EPS of $0.12, followed by a more substantial increase to $2.25 in 2022 and finally reaching $5.5 in 2023. This translates to a CAGR of approximately 31% for EPS from 2019 to 2023, reflecting both operational improvements and the resurgence of travel demand.

Expedia has maintained a total assets grew from about $21.42 billion in 2019 to approximately $21.64 billion by the end of 2023, indicating stability in asset management. The company’s total liabilities have also seen minor fluctuations but remained manageable, with total liabilities reported at around $13 billion in 2023 compared to $13.7 billion in 2019. This stability is crucial as it allows Expedia to navigate through economic uncertainties while investing in growth opportunities.

Expedia’s management has expressed optimism regarding future growth prospects, driven by ongoing recovery trends in the travel sector and strategic investments in technology and customer experience enhancements. The company aims to leverage its strong brand presence and diversified offerings to capture market share as global travel continues to rebound.

Technical Analysis:

The stock is on a stage 2 markup (bullish) on the monthly chart, and getting to a double top (bearish) on the weekly chart. The daily chart shows slowing momentum and lots of resistance in the $159 zone, and the should should head lower to the $134 range in the next few days / weeks. Long term this would be a better entry for the stock.

Bull Case:

Diverse Product Offerings: The company offers a wide range of travel products and services, catering to both leisure and business travelers. This diversity helps to mitigate risks and capture opportunities in different market segments.

Strategic Acquisitions: The company has a history of successful acquisitions, such as Travelocity, Hotwire, and Orbitz, which have expanded its market reach and product offerings.

Bear Case:

Intense Competition: The online travel market is highly competitive, with major players like Booking Holdings, TripAdvisor, and Ctrip, as well as a variety of regional and niche travel agencies. This competition can put pressure on pricing, margins, and market share.

Rising Operating Costs: The company’s operating costs, such as marketing expenses, technology investments, and employee salaries, can increase over time, putting pressure on margins.

Dependence on Third-Party Suppliers: Expedia Group relies on third-party suppliers, such as airlines and hotels, for a significant portion of its inventory. Disruptions or failures in these suppliers can negatively impact the company’s operations.