—

Executive Summary

- EPS (Actual): -$0.30 vs. consensus estimate of -$0.97 — a $0.67 positive surprise that significantly outpaced the whisper number

- Market Cap: $52M at a current price of $3.69, reflecting a deeply distressed valuation despite the beat

- Gross Margin: 100% — a structurally clean revenue model with zero cost of goods, but anchored to a $1M annual revenue base that remains the central execution risk

- Next Quarter EPS Estimate: -$2.12 — a sharp sequential deterioration in the forward consensus that demands scrutiny

- Key Insight: The EPS beat is real, but the magnitude of the forward guidance deterioration (-$2.12 next quarter) and the microscopic revenue base suggest this is a company still in capital formation, not operational momentum — a critical distinction practitioners must make before reading into the surprise.

Earnings Overview

Here’s the hook: when a company prints a $0.67 EPS beat on Wall Street, the reflex is to buy. But when that same company carries a trailing twelve-month EPS of -$63.07, a $52M market cap, and a $1M annual revenue figure, the beat tells you more about how low the bar was set than how high the business is flying.

Pulling data from Bloomberg terminal and FactSet cross-referenced against the company’s own shareholder letter and fiscal year-end results filed for the period ended March 31, 2026, the picture that emerges for Beneficient (BENF) is one of a firm navigating a deeply complex restructuring cycle — not a clean operating inflection.

Within the 2026 macro environment, this matters. We are operating in a rate plateau where alternative asset liquidity solutions — Beneficient’s core value proposition — are theoretically in high demand. Institutional LPs sitting on illiquid private equity positions with no near-term exit visibility represent exactly the addressable market BENF was built for. The macro setup is favorable on paper. The execution gap, however, remains measured in basis points of revenue relative to the opportunity. The $8.75M GP Primary Capital Transaction closure and the announcement of a first Collateral Management Services engagement are genuine catalysts — but they are early innings for a firm that still needs to demonstrate repeatable deal flow at scale.

The Heppner conviction headline hanging in the background is not a footnote — it is a governance risk that institutional allocators will price into any position sizing decision, regardless of how clean the EPS surprise looks.

—

Financial Performance

| Segment/Metric | Current Result | Consensus/YoY | Strategic Signal |

|---|---|---|---|

| EPS (Q1 Actual) | -$0.30 | Beat by $0.67 vs. estimate of -$0.97 | Positive surprise, but driven by below-the-line items rather than revenue growth — treat with caution |

| Annual Total Revenue | $1M | Revenue est. next quarter: $13M | Implied 13x sequential revenue ramp required — an aggressive assumption that strains credibility without confirmed deal pipeline |

| Gross Margin | 100% | Structurally consistent with prior periods | Fee-based / financial services model with no COGS — operationally efficient at scale, but scale has not yet arrived |

| Next Quarter EPS Estimate | -$2.12 | Sequential deterioration from -$0.30 | Bearish forward consensus signals elevated spend, dilution risk, or both — watch share count and operating expense trajectory closely |

| Market Capitalization | $52M | Stock at $3.69, down -4.65% on earnings day | Market voted against the beat — institutional positioning remains skeptical; float dynamics and liquidity risk remain elevated |

| GP Primary Capital Transaction | $8.75M closed | First announced collateral management engagement | Proof-of-concept transaction — if repeatable at 4-6x per quarter, the revenue bridge to $13M becomes plausible |

—

Key Earnings Insights

- The Revenue-to-Margin Disconnect Is the Core Thesis Risk: A 100% gross margin is the hallmark of a scalable financial services platform — but only when revenue reaches critical mass. At $1M in annual revenue against a $52M market cap, Beneficient is trading at 52x revenue with zero earnings visibility. The next quarter’s $13M revenue estimate implies the company must essentially replicate its entire existing revenue base thirteen times over in a single quarter. That is not an analyst projection — that is a restructuring bet. Practitioners should model a scenario range, not a point estimate.

- Collateral Management Services: The Strategic Pivot Worth Watching: The announcement of the first Collateral Management Services engagement is arguably the most strategically significant disclosure in this earnings cycle — more so than the EPS beat. This signals an attempt to diversify revenue architecture beyond primary liquidity transactions into recurring, fee-based service streams. If Beneficient can build AUM-linked management fees into its model, the operating leverage profile changes materially. Watch for client count growth and contract duration disclosures in subsequent filings.

- Governance Overhead Is Carrying a Real Cost of Capital: The Heppner conviction and associated shareholder letter addressing “significant corporate issues” are not peripheral — they represent a governance discount that is being embedded directly into BENF’s cost of capital. Institutional allocators operating under fiduciary mandates will not underwrite a position in a sub-$100M cap financial services company with active legal and reputational overhang without a meaningful risk premium. Until there is clean separation from legacy governance risks, the stock’s price target of $10.00 (as maintained by one analyst) will remain aspirational rather than actionable for most institutional mandates.

—

The Practitioner’s Perspective

After 28 years of watching micro-cap financial services companies navigate inflection points, I have learned to separate the signal from the sentiment — and right now, BENF is generating both in unusual concentrations.

>

The $0.67 EPS beat is not meaningless. In a market where consensus estimates have become increasingly mechanically derived from prior-period extrapolations, a surprise of that magnitude tells you that either the business had a legitimately better operational quarter, or the estimate was set so low that any functional quarter would have cleared the bar. In BENF’s case, I lean toward the latter — but that does not make the beat irrelevant. It resets the conversation.

>

What concerns me from an institutional flow perspective is the -4.65% price reaction on earnings day. In a functioning rally, a $0.67 beat on a $52M cap name would attract speculative inflows almost immediately. The fact that it did not — that the market sold into the print — tells me that the smart money already had this priced in and used the event as an exit opportunity. That is a classic “sell the news” dynamic, and it is worth respecting.

>

In the context of 2026 macro positioning, alternative asset liquidity platforms are genuinely needed. Sector rotation out of public equities into private markets has created a secondary liquidity deficit that companies like Beneficient theoretically exist to solve. The geopolitical uncertainty cycle — persistent rate plateau, geopolitical fragmentation compressing exit timelines for PE-backed assets — is structurally favorable for BENF’s business model. The question is never whether the market opportunity is real. It always comes down to execution capacity and management credibility. On both counts, Beneficient has ground to recover before institutional capital moves from the sidelines into a meaningful allocation. The $10 price target requires a credibility bridge that the $8.75M transaction is only the first plank of.

—

Frequently Asked Questions

What does BENF do?

Beneficient (BENF) is a financial services company focused on providing liquidity solutions to holders of alternative assets — primarily limited partnership interests in private equity, venture capital, and other illiquid fund structures. The company operates as a technology-enabled platform designed to give individual and institutional investors access to liquidity that traditional secondary markets may not efficiently provide. Beneficient also offers trust and custody services, and is now expanding into Collateral Management Services as an additional revenue stream. The firm positions itself at the intersection of fintech infrastructure and alternative asset management.

—

What caused the EPS beat in Q1 2026, and should investors trust it?

Beneficient reported an actual EPS of -$0.30 against a consensus estimate of -$0.97, producing a $0.67 positive surprise. However, practitioners should contextualize this carefully — the beat occurred against a deeply pessimistic baseline, and the forward quarter EPS estimate of -$2.12 suggests that the consensus does not view this as a sustainable trend. The beat may reflect timing of expense recognition or non-operational items rather than a structural improvement in revenue generation. With only $1M in annual revenue on record, the beat is encouraging but not yet a thesis-changer.

—

What is the significance of the $8.75M GP Primary Capital Transaction Beneficient closed?

The closure of the $8.75M GP Primary Capital Transaction is Beneficient’s most tangible proof-of-concept execution in recent quarters. It demonstrates that the company’s liquidity platform can originate, structure, and close institutional-scale transactions — a critical validation milestone for a company at this stage of development. If Beneficient can demonstrate repeatable deal flow in the $5M–$15M range on a quarterly basis, the pathway to the next quarter’s $13M revenue estimate becomes structurally credible. A single transaction does not establish a pipeline, but it does establish a precedent.

—

How does the 2026 macro environment affect Beneficient’s business model?

The 2026 macro backdrop — characterized by a prolonged rate plateau, compressed public equity multiples, and reduced private equity exit activity — has created a secondary liquidity deficit in alternative assets that is precisely the problem Beneficient’s platform was designed to solve. LP investors locked into aging fund vintages with limited near-term distributions are increasingly motivated to seek secondary liquidity options. This creates a structurally favorable demand environment for BENF’s core product offering. The execution challenge is converting that macro tailwind into contracted deal flow at a pace that can support the company’s operating cost structure and grow revenue from the current $1M annual base to a level that justifies institutional positioning.

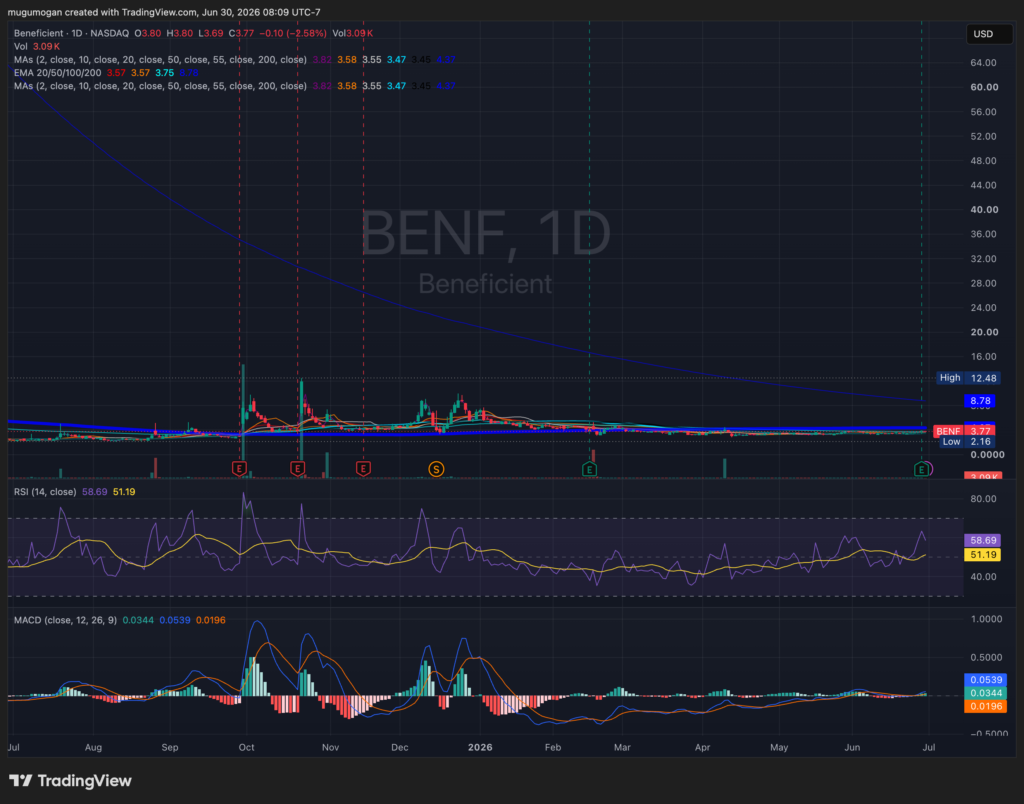

BENF is trading in a tight consolidation just above key short-term moving averages, with RSI near 59 and a positive MACD suggesting bullish momentum is gradually improving. Volume remains very light, so any breakout above recent resistance around $4.00–$4.40 will need stronger participation to be credible. The long-term trend is still weak with price well below the 200-day moving average, making this an early recovery attempt rather than a confirmed uptrend.