Executive Summary:

Sunrun is a leading provider of residential solar power systems in the United States. The company offers a variety of solar and energy storage solutions, including solar panel installation, battery storage systems, and home energy management services. Sunrun’s mission is to create a planet run by the sun by making solar energy more accessible and affordable for homeowners. Sunrun also aims to empower homeowners with clean energy solutions that can help them save money on their energy bills and reduce their carbon footprint.

Sunrun Inc. reported a revenue of $537.17 million, a decrease of 4.62% compared to the same period last year. The earnings per share (EPS) was -$0.37, higher than the consensus estimate of -$0.14, representing a 164.29% negative surprise.

Stock Overview:

| Ticker | $RUN | Price | $9.26 | Market Cap | $2.08B |

| 52 Week High | $22.26 | 52 Week Low | $8.22 | Shares outstanding | 224.34M |

Company background:

Sunrun Inc. is a leading provider of residential solar power systems in the United States. Founded in 2007 by Lynn Jurich, Ed Fenster, and Nat Kreamer, the company pioneered a subscription-based model for solar energy, allowing homeowners to access clean energy without the upfront cost of system ownership.

The company offers a comprehensive suite of solar and energy storage solutions, including solar panel installation, battery storage systems, and home energy management services. Sunrun’s focus on customer experience and long-term partnerships has driven its growth and established it as a major player in the residential solar market.

Sunrun faces competition from other solar providers such as Tesla, Vivint Solar, and Sunnova Energy. The company’s headquarters is located in San Francisco, California.

Recent Earnings:

Sunrun Inc. released its revenue for the quarter came in at $537.17 million, marking a 4.62% decline compared to the same period in the previous year.

Sunrun reported an EPS of -$0.37, a significant improvement compared to analyst expectations of -$0.14.

Their customer agreements and incentives revenue, demonstrated growth, increasing by 28% year-over-year to $405.9 million. Solar energy systems and product sales revenue declined by 47% to $131.3 million.

The Market, Industry, and Competitors:

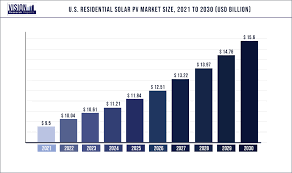

Sunrun operates in the rapidly growing residential solar energy market. This market is driven by several factors, including increasing electricity prices, growing environmental concerns, and government incentives promoting renewable energy adoption. The market is characterized by intense competition from established players like Tesla and newer entrants.

The global market to reach US$ 212.81 billion by 2030, exhibiting a compound annual growth rate (CAGR) of 17.9% during the forecast period. This growth is attributed to factors such as declining costs of solar PV systems, supportive government policies, and advancements in solar technologies.

Unique differentiation:

Tesla: A major player with strong brand recognition and vertically integrated operations, including battery production. Tesla’s entry has intensified competition, particularly in the premium segment.

Vivint Solar: A prominent player known for its door-to-door sales and strong customer service.

Sunnova Energy: A leading residential solar and energy storage provider with a focus on customer financing options.

Other regional and local players: Numerous smaller companies compete regionally, offering localized expertise and competitive pricing.

- Solar-as-a-Service Model: Sunrun pioneered the concept of leasing solar panels, allowing homeowners to access clean energy without the upfront cost of system ownership. This model has made solar energy more accessible to a wider range of customers.

- Comprehensive Service Offerings: The company offers a wide range of products and services, including solar panel installation, battery storage systems, home energy management services, and financing options. This comprehensive approach addresses the diverse needs of homeowners and strengthens customer loyalty.

Sunrun has established itself as a leader in the residential solar market and continues to innovate to maintain its competitive edge.

Management & Employees:

- Mary Powell: Chief Executive Officer

- Paul Dickson: President and Chief Revenue Officer

- Patrick Jobin: Senior Vice President of Finance and Investor Relations

- Rachit Srivastava: Head of Artificial Intelligence

- Patrick Kent: Chief Field Operations Officer

- Lynn Jurich: Co-Founder and Executive Co-Chair of the Board

Financials:

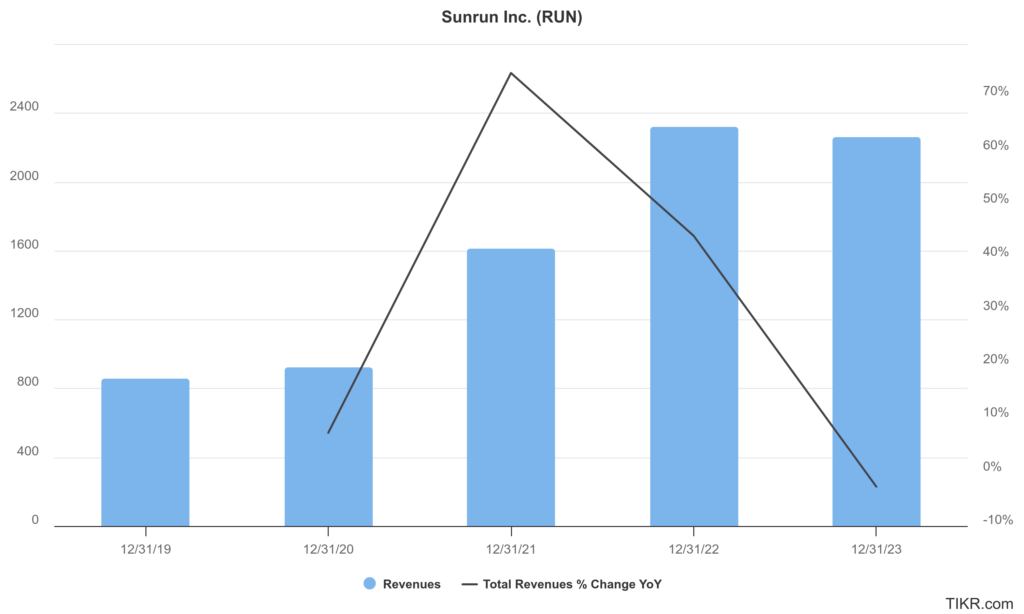

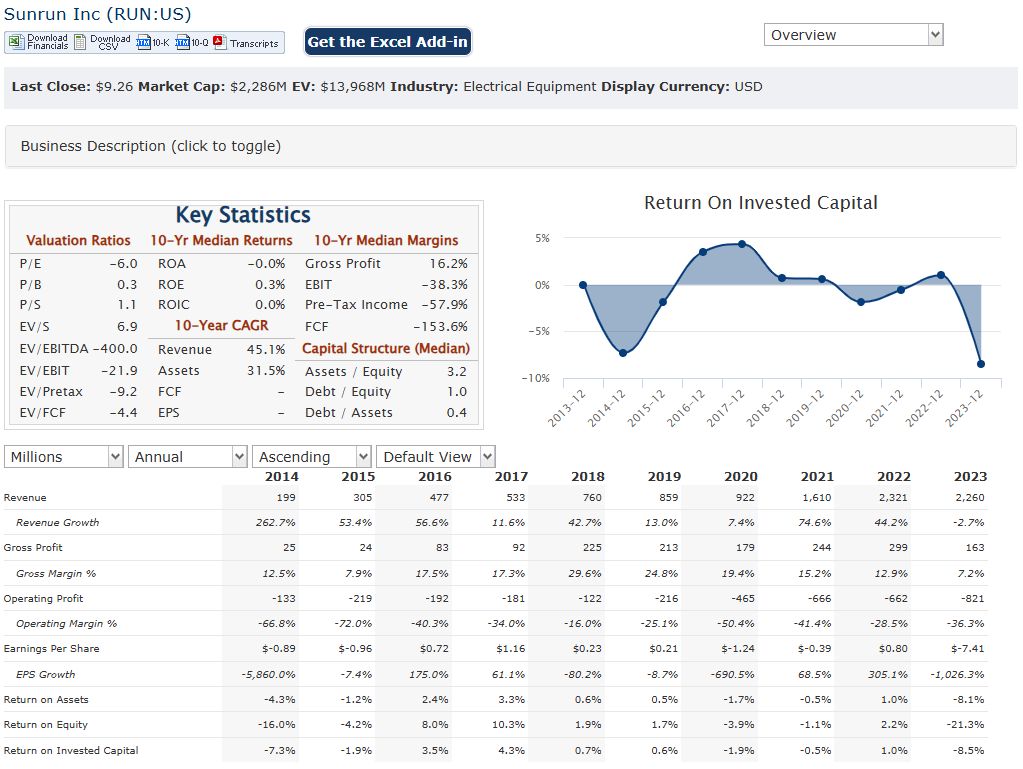

Sunrun Inc. has reported a compound annual growth rate (CAGR) in revenue of approximately 23.6%, with total revenue increasing from $858.6 million in 2019 to $2.26 billion in 2023. The growth trajectory has not been linear; after a substantial increase of around 74.6% from 2020 to 2021, the revenue saw a slight decline of about 3% in 2023 compared to the previous year, reflecting challenges in maintaining momentum amidst changing market conditions and competition.

The company recorded a net income of approximately $26 million, but this shifted to a loss of about $1.6 billion by 2023. The earnings per share (EPS) also reflected this downward trend, moving from $0.21 in 2019 to a loss of $7.41 in 2023. The CAGR for earnings over this period is negative, highlighting the company’s struggles to achieve consistent profitability despite increasing revenues.

Sunrun reported net earning assets exceeding $5 billion, which indicates a solid asset base despite its financial losses. The company has also seen its debt levels rise, with leverage ratios indicating high debt relative to EBITDA, which raises concerns about long-term financial sustainability. This is evidenced by a debt-to-EBITDA ratio that has escalated from -82.14x in 2019 to projections of around 76.41x by 2025.

Sunrun projected financial performance suggests cautious optimism with expected revenues for 2024 around $2.05 billion and an anticipated recovery trajectory as it aims for positive cash generation between $350 million and $600 million by 2025.

Technical Analysis:

The stock is in a markdown stage 4 (bearish) on the monthly and weekly charts, but in a consolidation, stage 1 phase on the daily chart. The near term outlook is towards the lows of $8 range. We would avoid this stock.

Bull Case:

Strong Market Position: Sunrun is a well-established leader in the residential solar market with a strong brand, a large customer base, and a comprehensive suite of products and services.

Potential for Improved Profitability: The company is focused on improving its profitability and navigating the challenging economic environment.

Bear Case:

Economic Uncertainty: Rising interest rates and potential economic downturns could impact consumer demand for solar installations, as homeowners may prioritize other expenses.

Execution Risks: Sunrun faces challenges in executing its growth strategy, including scaling its operations, managing customer acquisition costs, and integrating new technologies.

Regulatory Risks: Changes in regulatory policies related to solar energy, grid integration, and energy storage could create uncertainty and impact the company’s operations.