Company Overview

Levi Strauss & Co. (Levi) is a global apparel company best known for its Levi’s® denim brand, along with ancillary brands such as Dockers® and more recently Denizen® and Signature by Levi Strauss. It designs, sources, markets, and distributes jeans, casual wear, and accessories for men, women, and children. Over recent years, Levi has emphasized a shift toward direct-to-consumer (DTC) channels, positioning its retail and e-commerce networks as a greater share of overall sales. Its distribution spans wholesale partners, own retail stores, and digital platforms. Despite apparel industry cyclicality, Levi benefits from strong brand recognition, global reach, and efforts to optimize its product and channel mix.

Most Recent Earnings & Guidance

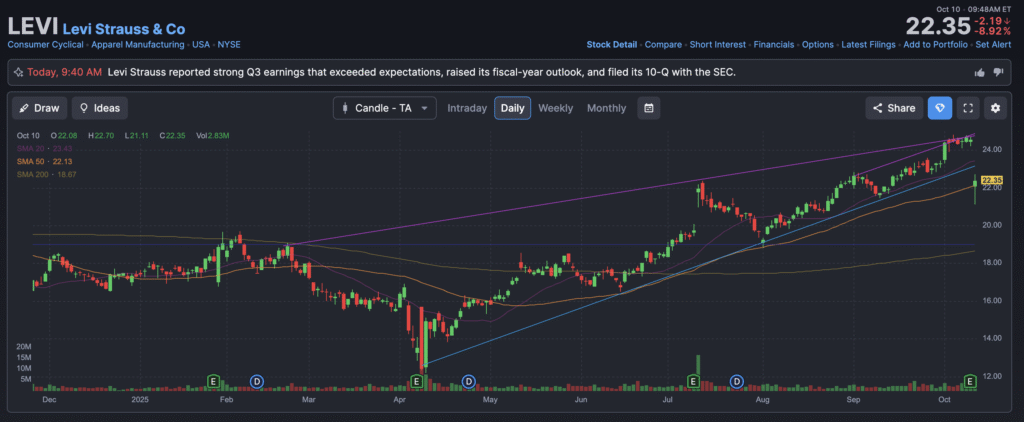

In its Q3 2025 (fiscal) results announced October 9, 2025, Levi reported adjusted EPS of $0.34 and net revenue of $1.54 billion, representing year-over-year revenue growth of ~7%, both of which beat consensus estimates. The company modestly raised its full-year adjusted EPS guidance to a range of $1.27 to $1.32 per share, though that midpoint remains slightly below the ~$1.31 market consensus. Levi cautioned that U.S. import tariffs would weigh on its fourth-quarter gross margins by about 130 basis points.

For the broader 2025 fiscal year, Levi expects revenue growth of about 3% and reiterated efforts in inventory management, pricing discipline, and continued growth in DTC sales.

Founding, Business Model & Products, Competitors, Headquarters

Levi’s origins trace back to 1853, when Levi Strauss, a German immigrant, founded a dry-goods business in San Francisco during the Gold Rush era. Over time, Strauss and tailor Jacob Davis pioneered denim work pants reinforced with rivets, leading to the iconic Levi’s blue jeans. The company remained private (under family control or private equity) until its IPO in March 2019, when it raised ~$550 million.

Today, Levi’s product portfolio includes denim (jeans, jackets), casual wear (shirts, tops, outerwear), accessories, and licensed products under Levi’s, Dockers, Beyond Yoga (fitnesswear), and more. Levi has recently trimmed or exited non-core or underperforming sub-brands (e.g. Denizen) to streamline its focus.

Its headquarters is in San Francisco, California, while its design, sourcing, distribution, and retail footprint is global.

Key competitors include denim and general apparel brands such as Wrangler, Lee, GAP, Calvin Klein, Diesel, True Religion, PVH / Tommy Hilfiger, and others.

In the broader apparel/denim market, Levi competes on brand equity, product fit and design, channel reach (especially DTC), supply chain efficiency, and pricing against both heritage denim brands and newer fast-fashion or specialty apparel players.

Market Landscape & Growth Outlook

Levi operates primarily in the global apparel and denim market, overlapping with casualwear, fashion, and lifestyle segments. The denim market remains mature but has seen renewed interest in “heritage” and premium denim, as well as trends around sustainability, fit innovation, and fashion cycles. On the broader apparel side, competition is fierce from fast fashion, athleisure, and digitally native brands.

Analysts expect modest growth in apparel markets, particularly in developed geographies, with emerging markets offering higher growth potential. The denim niche may grow in low-single digits annually, but premium/brand-driven segments could outperform.

By 2030, projections for the global apparel market generally imply a CAGR in the 3–5% range, though denim-specialty growth may lag or modestly exceed that depending on consumer preferences, inflation, and material cost pressures. Levi’s pivot toward value-add branding, channel shift, and margin improvements are attempts to outperform a more commoditized base market.

Competitors

Among Levi’s most direct competitors in the denim/apparel space are Wrangler and Lee (heritage denim brands), Gap Inc. (through its brands like Old Navy and Gap), PVH / Tommy Hilfiger / Calvin Klein, and premium fashion brands like Diesel.

In adjacent space, broader apparel and fashion brands (fast-fashion, athleisure, digital-first labels) also compete for share of consumer spending, which pressures Levi’s on marketing, product innovation, and channel economics.

Unique Differentiation

- Brand heritage & equity: Levi has deep brand recognition, especially in denim, which allows premium pricing and loyalty.

- DTC emphasis: Its increasing proportion of direct-to-consumer sales gives higher margins, data insights, and customer control, insulating somewhat from wholesale volatility.

- Channel & inventory discipline: Levi’s efforts to tighten inventory management, more full-price selling (less discounting), and efficient supply chain are intended to preserve margins in tougher cost environments.

- Portfolio focus: By shedding underperforming brands and focusing around core Levi’s denim + casual lifestyle, the company simplifies its value proposition and cost structure.

- Global sourcing flexibility: Levi’s global sourcing footprint and diversified manufacturing and supply strategy help manage trade/tariff risks relative to more concentrated peers.

Management Team

- Michelle Gass (CEO) – She assumed the CEO role in early 2025 (after Chip Bergh transitioned) and is steering Levi through its brand and channel transformation.

- Harmit Singh (CFO & Chief Growth Officer) – He leads finance and growth functions, including guiding margin outlook, capital allocation, and forecasting.

- (A third name is less publicly emphasized currently) – The company’s investor materials often highlight the CEO and CFO as the core executive drivers of strategy and operations.

Financial Performance (Last 5 Years)

Over the past five years, Levi has faced cyclical headwinds, but delivered moderate top-line growth and margin recovery in more recent periods. Revenue growth has generally been in the low- to mid-single digits, with occasional quarters of stronger growth aided by brand refreshes or favorable fashion trends. The shift to DTC has boosted gross margins and operating leverage over time.

Earnings growth has been more volatile, influenced by swings in costs (raw materials, trade/tariff impact, logistics) and discounting. In favorable periods, adjusted EPS growth outpaced revenue growth. But periods of margin compression or restructuring have led to swings.

On the balance sheet, Levi has maintained reasonable leverage; capital expenditures are moderate (reflecting retail, IT, logistics investments), and inventory metrics have been a key focus. The company’s working capital and inventory management have become more disciplined, reducing excess to protect margins.

In recent quarters especially, the margin expansion and improved full-price sell-through have shown the model’s leverage when conditions are favorable. The company’s debt levels remain manageable relative to cash flows, giving some flexibility, though macro downturns or cost inflation pose risks.

Bull Case

- Strong brand equity allows pricing power and margin resilience.

- Continued shift to DTC and retail efficiencies could unlock margin expansion.

- Effective mitigation of trade/tariff and cost pressures (via sourcing, efficiency) may allow earnings growth even in a challenging environment.

Bear Case

- Tariff escalation, input cost inflation, or supply chain disruption could erode margins heavily.

- Consumer discretionary pressure (especially on apparel) could weaken demand, particularly in wholesale channels.

- Competitive pressures from fast-fashion or digitally native brands may erode share and force discounting.

The stock is in a stage 2 bullish markup on the monthly and weekly chart, but moved to a consolidation stage 3 and likely going to a bearish stage 4 on the daily chart. The near term outlook is to the negative and should reach lower to $20 range.