Corpay Inc. (NYSE: CPAY) is a global corporate payments company that provides businesses and consumers with streamlined solutions to manage and pay expenses efficiently. The company’s suite of services includes vehicle-related payments, lodging expenses, and corporate payments, operating across the United States, Brazil, the United Kingdom, and other regions. As of 2024, Corpay reported revenues of $4.0 billion and adjusted net income of $1.4 billion, serving over 800,000 business clients.

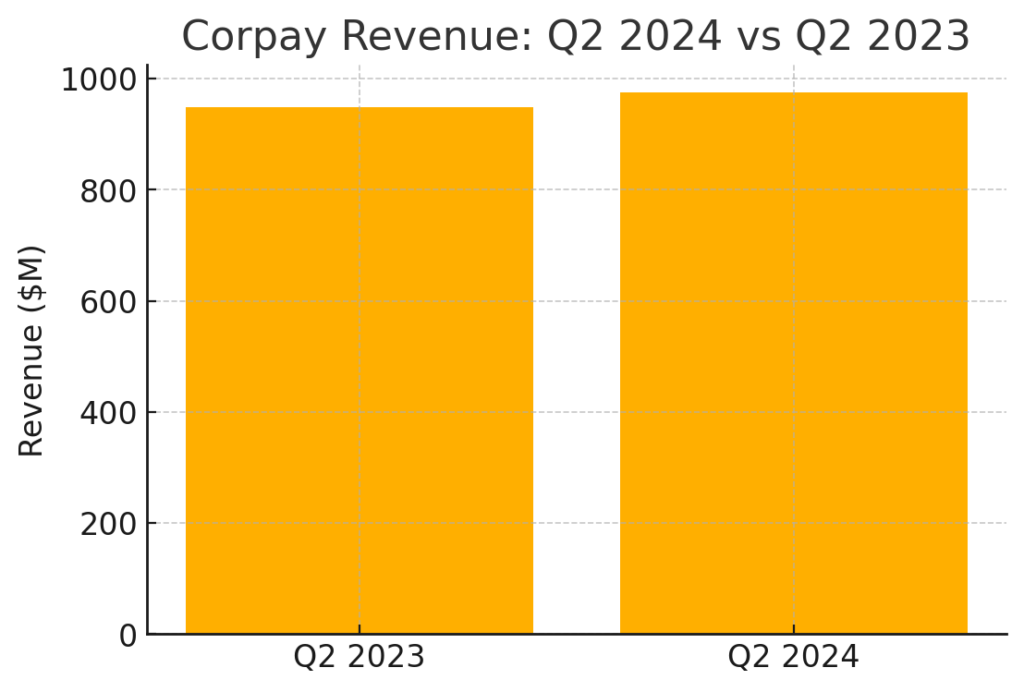

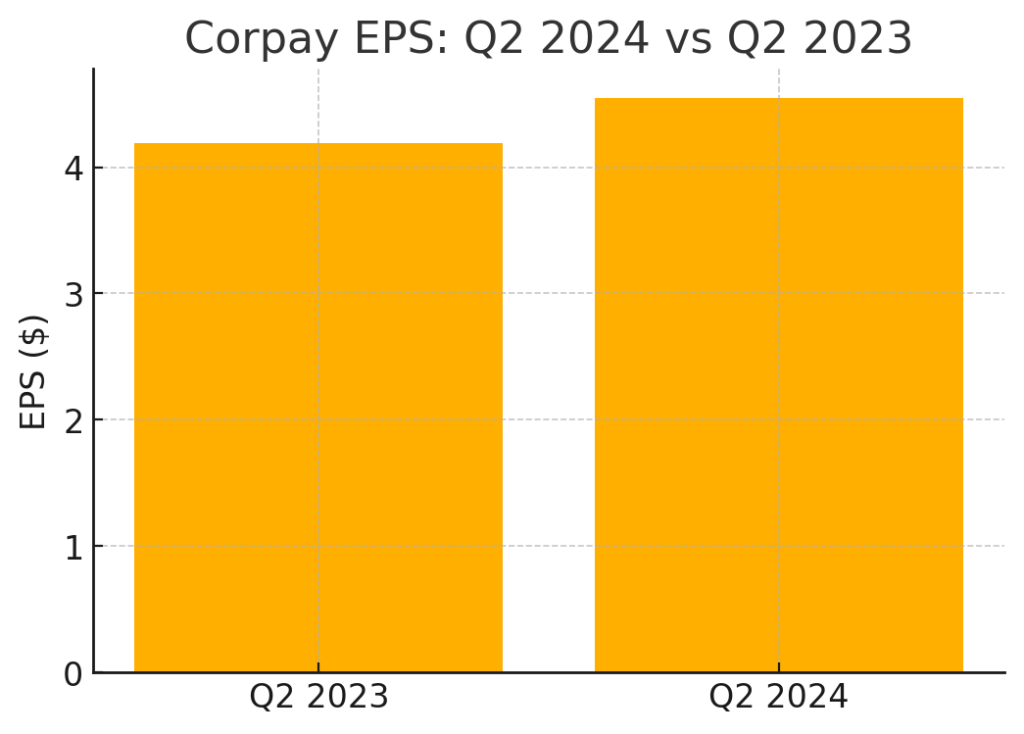

Corpay Inc. (NYSE: CPAY) reported its second-quarter 2024 financial results with revenues reaching $975.7 million, a 3% increase from the same quarter in 2023. Adjusted earnings per share (EPS) rose 8% year-over-year to $4.55, surpassing analyst expectations of $4.51. Net income grew by 5% to $251.6 million, and the company achieved an EBITDA of $517.7 million, reflecting a 4% increase from the previous year. These results indicate steady growth and operational efficiency.

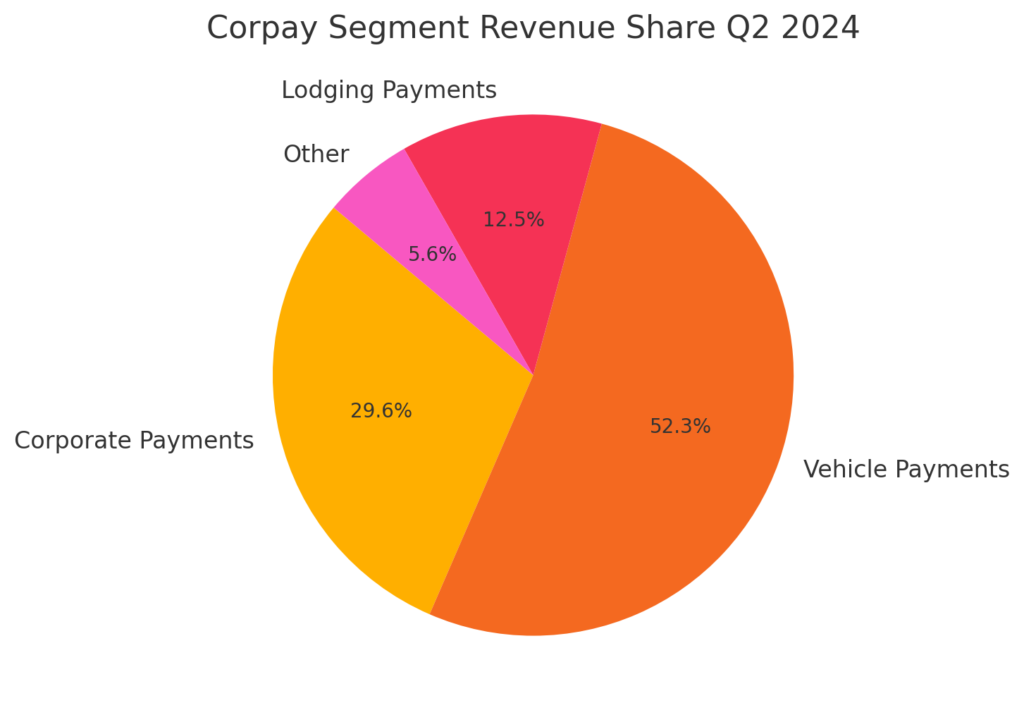

Breaking down the revenue by segments, Corporate Payments led with a 17% year-over-year increase to $289 million, accounting for approximately 30% of total revenue. Vehicle Payments generated $510.3 million, a modest 1% increase.Lodging Payments experienced a 10% decline to $122 million, while the Other segment, including Gift and Payroll Card operations, saw a slight decrease of 2% to $55 million. The strong performance in Corporate Payments underscores the company’s strategic focus on this segment.

For the third quarter of 2024, Corpay projects revenues between $1.015 billion and $1.035 billion, with adjusted EPS ranging from $4.90 to $5.00. The company maintains its full-year 2024 revenue guidance between $3.975 billion and $4.025 billion, and adjusted EPS between $18.85 and $19.15. These projections reflect confidence in continued growth, particularly in the Corporate Payments segment.

Corpay’s stock has demonstrated resilience, with a significant appreciation over the past year. Following the Q2 earnings release, the stock experienced a modest decline in after-hours trading, reflecting investor caution amid broader market volatility. However, the company’s inclusion in Time magazine’s “World’s Best Companies” list and recognition by institutional investors highlight its strong market position.

Competitors

Corpay faces competition from various companies offering payment and expense management solutions. Key competitors include Ramp, BILL AP/AR, BILL Spend & Expense (formerly Divvy), Tipalti, and Pleo. These companies provide similar services, such as AP automation, spend management, and expense tracking, catering to businesses of different sizes and industries.

Despite the competitive landscape, Corpay differentiates itself through its extensive global reach, diverse product offerings, and strategic acquisitions that enhance its service capabilities.

Unique Differentiation

Corpay’s unique differentiation lies in its comprehensive and integrated suite of payment solutions that cater to various business needs, including vehicle payments, lodging, and corporate expenses. The company’s strategic acquisitions, such as Paymerang and its investment in AvidXchange, have expanded its capabilities in AP automation and accounts payable services. Additionally, Corpay’s global presence and large client base provide it with a competitive edge in the corporate payments industry.

Bull Case for Corpay Stock

- Strong Market Position: Corpay’s comprehensive suite of payment solutions and global presence position it well to capitalize on the growing demand for corporate payment services.

- Strategic Acquisitions: The company’s acquisitions, such as Paymerang and investment in AvidXchange, enhance its capabilities in AP automation and expand its market reach

- Consistent Financial Growth: Corpay has demonstrated steady revenue and net income growth over the past five years, reflecting its operational efficiency and strategic execution.

Bear Case for Corpay Stock

Integration Risks: The company’s growth strategy involves multiple acquisitions, which may present integration challenges and operational complexities.

High Debt Levels: With a debt-to-equity ratio of 254.3%, Corpay’s high leverage could pose risks, especially in a rising interest rate environment.

Competitive Market: The corporate payments industry is highly competitive, with numerous players offering similar services, potentially impacting Corpay’s market share and pricing power

The stock is in a stage 4 decline (bearish) on the monthly chart, but reversal in place for a stage 2 markup (bullish) on the weekly chart. The daily chart is in bullish stage 2 as well, with a move to $347 most likely