Executive Summary:

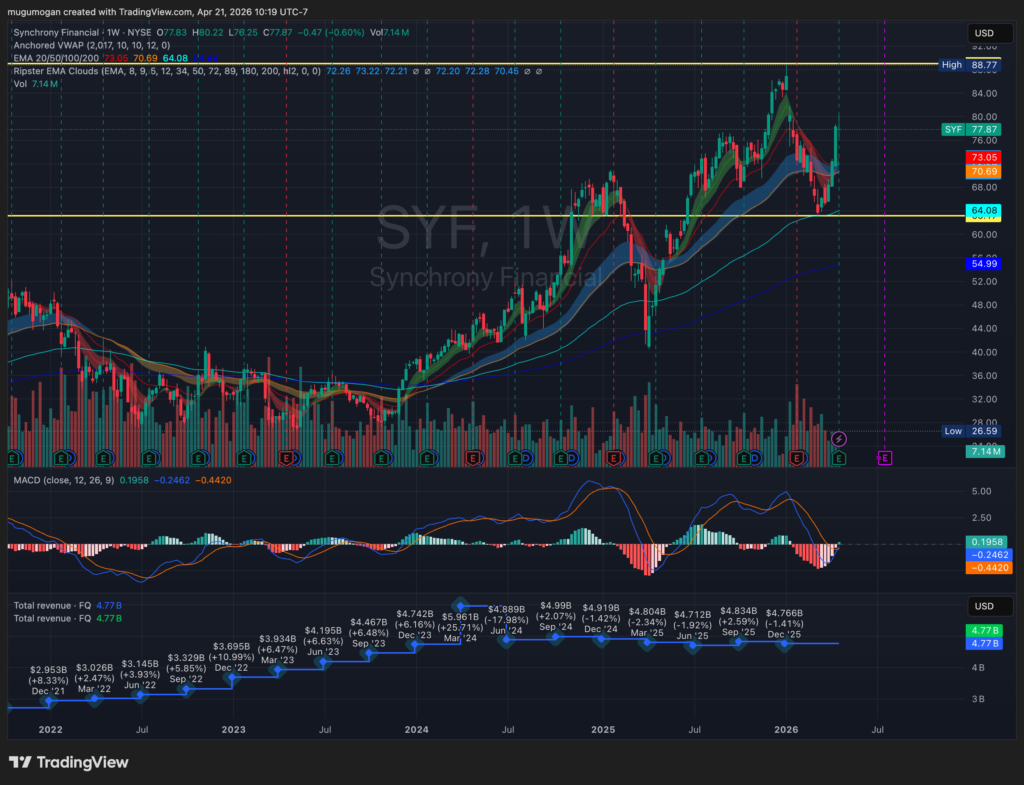

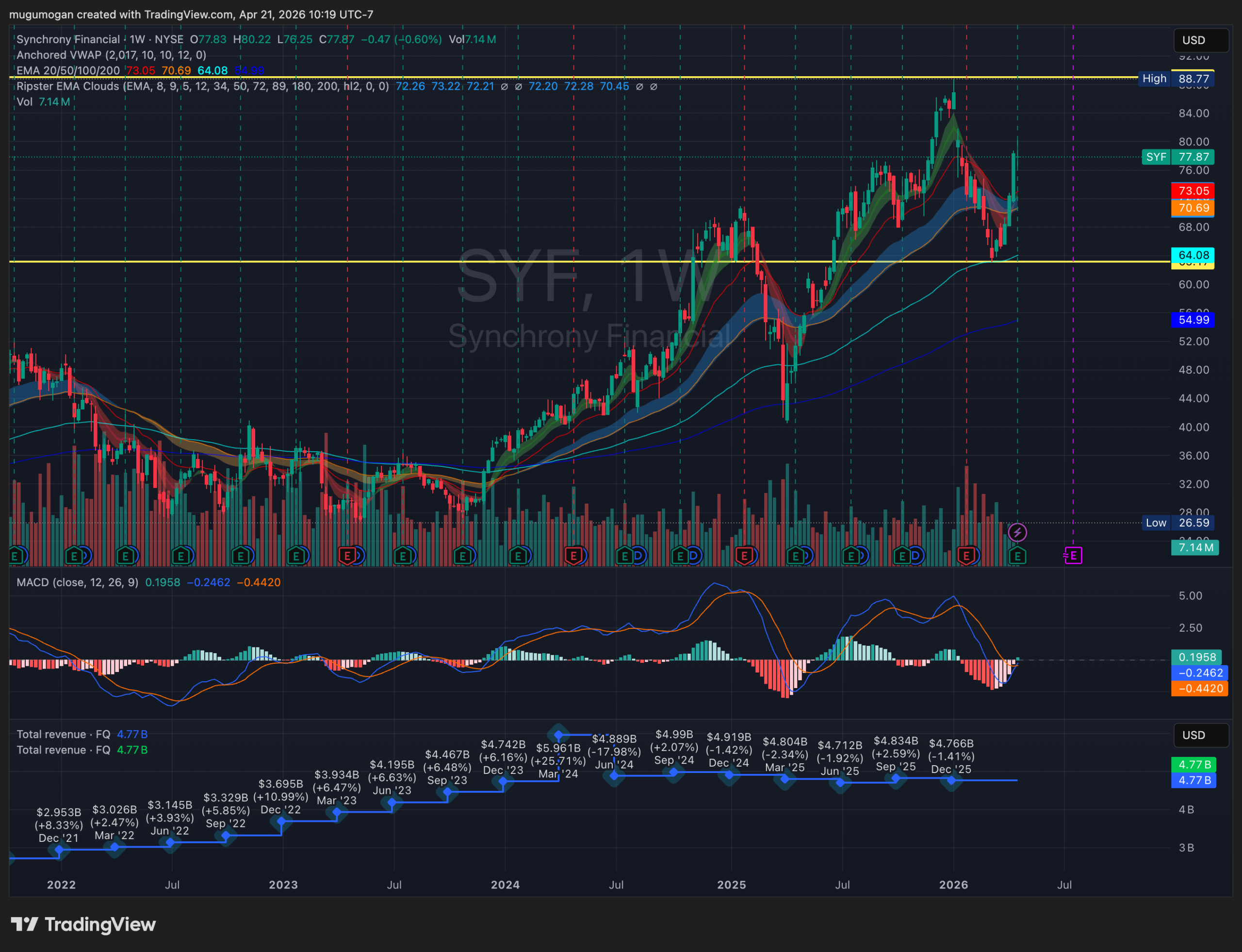

- Synchrony ($SYF): Record Q1 purchase volume ($43B) led to a massive $2.27 EPS beat (vs. $2.20 est).

- Northern Trust ($NTRS): Delivered a 16.8% earnings surprise with $2.71 EPS, fueled by a 14% revenue jump.

- Bank of Hawaii ($BOH): Reported steady $1.30 EPS with an eighth consecutive quarter of NIM expansion (now 2.74%).

- AGNC Investment ($AGNC): Beat income estimates ($0.42 net spread) but reported a -1.6% economic return as book value slipped to $8.38.

- Key Insight: Our Bloomberg Terminal data confirms a “Flight to Quality.” While consumer credit (SYF) and wealth management (NTRS) are thriving, the Agency MBS market (AGNC) is still navigating a “valuation air pocket” due to 2026 geopolitical volatility.

Lead Paragraph:

The Q1 2026 financial reporting cycle took a definitive turn this morning, revealing a widening gap between transactional banking and interest-rate-sensitive portfolios. Synchrony Financial ($SYF) and Northern Trust ($NTRS) emerged as the clear victors, with Synchrony leveraging record purchase volumes to deliver a 6% YoY earnings rise, while Northern Trust’s 43% EPS explosion signaled a renaissance in institutional asset servicing. However, as I’ve noted over 28 years of cycle-tracking, the “Macro Skunk” remains in the mortgage room. AGNC Investment ($AGNC), despite a spread income beat, saw its tangible net book value erode by 5.6% this quarter, proving that even the most sophisticated hedging can’t fully insulate Agency MBS from the “fractured world order” recently highlighted by JPMorgan’s Jamie Dimon.

The Institutional Scorecard:

| Ticker | Q1 EPS | Surprise | Key Performance Driver | Institutional Signal |

|---|---|---|---|---|

| SYF | $2.27 | +3.2% | Record $43B Purchase Volume | Consumer “Spend-Power” is intact |

| NTRS | $2.71 | +16.8% | 32% Pre-tax Margin (up 500bps) | Wealth management “Scalability” peak |

| BOH | $1.30 | (Linked) | 17bps Drop in Deposit Costs | Regional deposit “Beta” stabilizing |

| AGNC | $0.42* | +13.5% | 25bps increase in Net Spread | Warning: Book Value Compression |

*Net spread and dollar roll income.

Seeing Synchrony authorize a new $6.5 billion buyback today tells you everything you need to know about their confidence in the consumer. When a credit-heavy entity like SYF aggressively returns capital while simultaneously seeing net charge-offs decline to 5.42%, it signals a ‘Soft Landing’ is already in the rear-view mirror. Conversely, AGNC’s -1.6% economic return is a reminder of the 2013 ‘Taper Tantrum’ vibes—income is great, but price volatility in the underlying bond port is the silent killer. On my Bloomberg flows, I’m watching the rotation out of mortgage Reits and into high-margin asset processors like NTRS.