BlackBerry is a Canadian-based software and cybersecurity company that has fully transitioned away from its legacy smartphone business into enterprise security and embedded systems. The company operates primarily through two segments: Secure Communications (cybersecurity, UEM, and endpoint security) and IoT (QNX software used in automotive and embedded systems). BlackBerry’s software is embedded in over 235 million vehicles globally, giving it a strong footprint in automotive operating systems. Its strategy focuses on mission-critical security, government-grade encryption, and embedded software for regulated industries. Despite strong positioning, the company has struggled to return to consistent revenue growth, making it a turnaround story.

Latest Earnings (Reported Today) — Profitability Improving, Growth Still Missing

BlackBerry reported Q1 FY2026 revenue of ~$173M (↓ ~7% YoY, ahead of expectations) with adjusted EPS of ~$0.03 (vs ~breakeven expected). The upside came from better cost control and operating leverage, particularly in the Secure Communications segment, which stabilized after prior declines. The IoT/QNX segment remained steady with continued automotive design wins, but revenue growth remains muted due to long production cycles. Management guided for flat to slightly down revenue in the near term, while emphasizing continued margin expansion. The key takeaway: BlackBerry is executing on profitability, but top-line growth remains the missing piece.

Company History, Products, and Strategic Evolution

BlackBerry was founded in 1984 by Mike Lazaridis and Douglas Fregin in Waterloo, Canada, originally as Research In Motion (RIM). It became globally dominant in the 2000s with its secure mobile devices before losing relevance to Apple and Android ecosystems. Under CEO John Chen (2013–2023), the company pivoted away from hardware into software and cybersecurity through acquisitions like Cylance. Today, BlackBerry focuses on enterprise security, endpoint management, and embedded operating systems, shedding its legacy identity entirely. Its transformation is one of the most well-known pivots in tech, though execution has been uneven.

The Secure Communications segment includes endpoint security, unified endpoint management (UEM), and secure messaging solutions used by governments and enterprises. BlackBerry’s cybersecurity offerings emphasize AI-driven threat detection and compliance-heavy environments. However, competition from larger players has limited its growth trajectory in recent years. The segment has recently stabilized but is not yet delivering strong expansion.

The IoT division, powered by QNX, is a real-time operating system widely used in automotive infotainment, digital cockpits, and ADAS systems. BlackBerry has deep partnerships with OEMs and Tier 1 suppliers, making it a critical embedded software provider. While design wins remain strong, revenue realization lags due to long automotive production cycles. This creates a disconnect between backlog strength and reported revenue growth.

Market Opportunity — Cybersecurity and Automotive Software Growth

The global cybersecurity market is expected to exceed $500B by 2030, growing at a CAGR of ~12–14%, driven by increasing digital threats and regulatory requirements. BlackBerry operates in endpoint security and UEM, but faces intense competition from larger, faster-growing vendors. Its niche strength lies in highly regulated industries such as government, defense, and financial services. However, it lacks the scale and innovation pace of leading cybersecurity firms.

The automotive software market, particularly for embedded operating systems and ADAS platforms, is expected to grow at a CAGR of ~15–20% through 2030. With millions of vehicles already running QNX, BlackBerry has a strong installed base advantage. The shift toward software-defined vehicles and autonomous systems is a long-term tailwind. However, monetization depends heavily on OEM production cycles and platform adoption rates.

Competitive Landscape — Strong Rivals Across Both Segments

In cybersecurity, BlackBerry competes with companies like CrowdStrike, Microsoft, and Palo Alto Networks, all of which have significantly larger scale and faster innovation cycles. These competitors offer broader platforms, better ecosystem integration, and stronger growth momentum. BlackBerry’s differentiation is security certification and legacy enterprise relationships, but that has not translated into market share gains.

In IoT/automotive, QNX competes with Linux-based systems, Android Automotive, and proprietary OEM platforms. While QNX is known for reliability and safety certifications, open-source alternatives are gaining traction. Large tech companies entering automotive software also increase competitive pressure.

Differentiation — Security + Embedded Systems Niche

BlackBerry’s key differentiation lies in its combination of government-grade cybersecurity and embedded operating systems. Its software is trusted in mission-critical environments where reliability and compliance matter more than cost. The QNX platform’s dominance in safety-critical automotive systems is a major asset. However, differentiation alone has not translated into strong financial performance, which remains the core issue.

Management Team — Transition Leadership

John J. Giamatteo, the current CEO, previously led BlackBerry’s cybersecurity division and is focused on stabilizing growth and improving profitability. His strategy emphasizes cost discipline, core product focus, and monetizing existing assets. The leadership team is largely execution-focused rather than innovation-driven at this stage. The priority is turning BlackBerry into a sustainable, profitable software company.

Financial Performance — 5-Year View Shows Stagnation

Over the past five years, BlackBerry’s revenue has declined from over ~$1B annually to the ~$600–700M range, reflecting divestitures and weak organic growth. The company has struggled to replace declining legacy revenue streams with high-growth software revenue. This lack of growth is the primary reason for investor skepticism.

Earnings performance has improved recently due to aggressive cost cutting and restructuring efforts. BlackBerry has moved closer to consistent profitability, with recent quarters showing positive adjusted EPS. However, these gains are largely margin-driven rather than revenue-driven.

The balance sheet remains relatively stable, with manageable debt levels and sufficient liquidity. BlackBerry has focused on conserving cash and optimizing operations rather than aggressive expansion. This conservative approach supports the turnaround but limits growth acceleration.

Overall, the financial story is clear: declining revenue, improving margins, but no sustained growth engine yet.

Bull Case

- Margin expansion continues, leading to consistent profitability and cash flow

- QNX benefits from software-defined vehicle adoption and converts backlog into revenue

- Cybersecurity segment stabilizes and returns to modest growth

Bear Case

- Continued revenue decline offsets margin improvements

- QNX growth remains slow due to long automotive cycles

- Cybersecurity loses further share to stronger competitors

Analyst Reactions — Mixed Sentiment

Initial analyst reactions were cautiously positive on the EPS beat and cost discipline, but concerns remain around revenue stagnation. Some analysts maintained neutral ratings, emphasizing the need for sustained top-line growth. Price targets largely remained unchanged, reflecting limited conviction in near-term upside. The consensus view: execution is improving, but growth visibility is still weak.

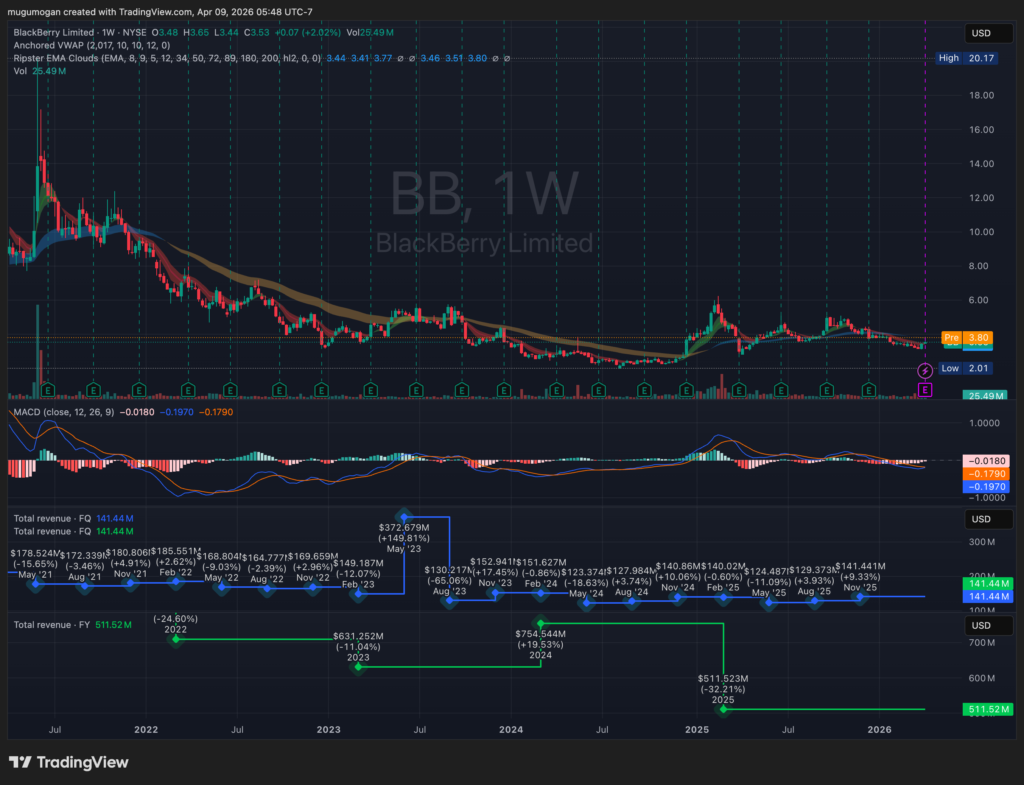

BlackBerry remains in a long-term downtrend with lower highs and weak momentum, despite some recent base-building around the $3–4 range. The stock is failing to break above key moving averages, and MACD is rolling over again, signaling lack of sustained buying pressure. Unless it reclaims the ~$4.5–5 resistance zone with volume, this continues to look like a range-bound or slow bleed rather than a breakout setup.