PayPal Holdings is a leading global technology platform that enables digital and mobile payments for consumers and merchants around the world. Founded (in its earlier forms) in the late 1990s and spun out as PayPal in 2015, the company had 2024 revenues of roughly $29.8 billion and has grown its payment-volume scale significantly in recent years. The company is headquartered in San Jose, California, and its top three competitors include Visa Inc., Mastercard Incorporated, and Square, Inc. (now Block, Inc.). The platform encompasses the PayPal branded wallet, Venmo, Braintree, Xoom and other services, driving digital commerce globally. Its mission emphasizes democratizing financial services and empowering people and businesses to join and thrive in the global economy.

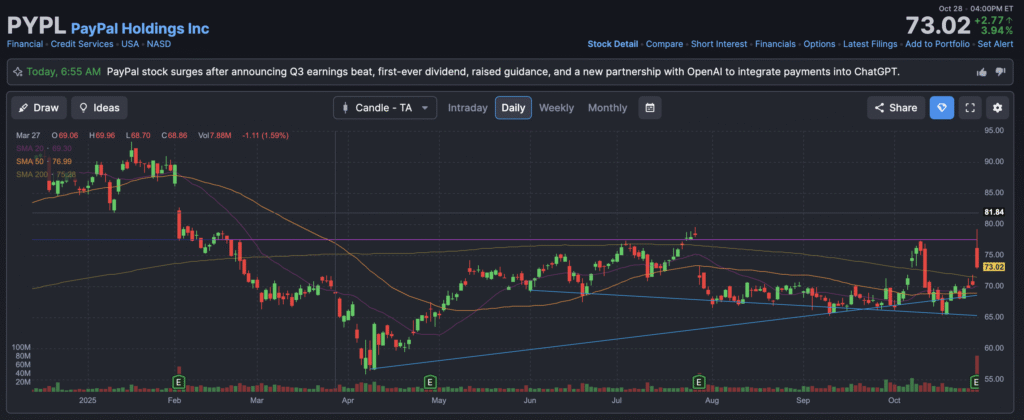

Earnings Released Yesterday (Oct 28, 2025) — PayPal reported a strong third‐quarter result. Revenue rose 7% year-over-year to approximately $8.4 billion. Earnings per share (adjusted) came in at $1.34 versus analyst expectations around ~$1.20. The company also raised its full-year adjusted EPS guidance to $5.35-$5.39, up from a prior range of $5.15-$5.30. Moreover, PayPal announced its first-ever dividend of $0.14 per share, signalling increased confidence in cash generation.

3. History, Founders, Funding, Products & Headquarters

PayPal’s roots trace back to Confinity (founded in 1998) and X.com, which merged and evolved into PayPal by around 2000. The company went public in 2002, was acquired by eBay, and then spun off into an independent publicly traded company in July 2015. Its founding team includes figures such as Max Levchin, Peter Thiel, Luke Nosek, Yu Pan and others. As a public company it has not been a “venture-funding” start-up in recent years in the traditional sense—its growth path has been driven by organic expansion and acquisitions (for example acquiring Xoom, Honey, iZettle). Its headquarters are located in San Jose, California. Product-wise, PayPal operates a digital wallet and payments network connecting consumers and merchants globally, offering merchant services, consumer payments, peer-to-peer transfers, credit and debit card products, and supporting global cross-border transactions. Key competitors include Visa, Mastercard, Square (Block), Stripe (private), Adyen, and other fintech payments players.

4. Market Dynamics and Growth Expectations

PayPal operates in the global digital payments market, encompassing e-commerce payments, peer-to-peer payments, merchant services, mobile wallets, and cross-border remittances. The total addressable market is enormous: global digital payments are projected to continue growing at a healthy compound annual growth rate (CAGR) towards 2030, with some estimates suggesting 10 %-15 %+ annual growth depending on region and segment as commerce increasingly shifts online. For PayPal specifically, growth drivers include increasing online penetration, rising digital wallet adoption, cross-border commerce expansion, and higher value-added services (merchant solutions, subscriptions, crypto). As of 2025 many markets remain under-penetrated, so the runway remains meaningful. Moreover, PayPal’s emphasis on transaction margin expansion (not just volume growth) suggests the growth opportunity is not just top-line scale but improving profitability.

5. Competitors

PayPal faces competition from major legacy payment networks such as Visa and Mastercard, which offer card-based networks and increasingly digital wallet solutions. In fintech, rivals include Block (formerly Square), Stripe (private but a large payments facilitator), Adyen, and other regional players (e.g., Worldpay/FIS, Global Payments). Each of these competitors has advantages: Visa/Mastercard have massive networks and brand strength; Stripe is developer-friendly and growth-oriented; Block has a strong SMB focus. In the digital wallet/peer-to-peer space, Venmo (part of PayPal) competes with Zelle, Apple Pay, Google Pay, and other emerging mobile wallet offerings.

6. Unique Differentiation

PayPal’s differentiation lies in its two-sided network connecting both consumers and merchants globally with scale, its multiple branded platforms (PayPal wallet, Venmo, Braintree, Xoom) allowing layered monetization (transaction revenue, merchant services, value-added services), and its global reach (serving more than 200 markets). Its brand recognition and trust in digital payments is strong. Furthermore, PayPal is increasingly focusing on high-margin services (branded checkouts, value-added merchant services) rather than relying purely on volume growth, which may provide an edge versus competitors still focused mostly on scale. The company’s global cross-border payment infrastructure and ability to integrate new services (crypto, digital wallets, merchant value-added solutions) further help differentiate.

7. Management Team (selected members)

Alex Chriss serves as President & Chief Executive Officer, having joined from Intuit where he led the small business and self-employed group, and officially took over as PayPal CEO in 2023. Under his leadership PayPal is pivoting toward profitability and value-added services. Dan Schulman previously served as CEO and remains on the board; his tenure saw PayPal through large growth phases including mobile wallet expansion. John Donahoe is the Chairman of the Board, bringing experience from leadership (e.g., at Nike, eBay) and focusing on governance, strategy and overseeing the board’s direction. These key executives anchor the company’s leadership and strategic direction.

8. Financial Performance Overview (last 5 years)

Over the past five years PayPal has grown steadily though not explosively. Revenue growth has been modest, reflecting maturing business and macro headwinds; for example full-year 2023 revenues were ~$29.8 billion, up from previous years by single‐digit to low-double-digit percentages. Earnings (net income) have similarly grown but with variability depending on investment, margin pressure, and macro factors. The revenue CAGR over the past five years is likely in the ~5-10 % range, while earnings growth could be a bit higher when margin improvements and cost controls are applied. On the balance sheet side, PayPal maintains a solid asset base and manageable liabilities; it has invested in share repurchases (announced $15 billion authorization) and is focused on returning capital and improving margin as growth slows. The company appears increasingly focused on optimizing profitability rather than purely aggressive growth, which aligns with its matured competitive position.

9. Bull Case

- PayPal can capitalize on its global payments network and scale, leveraging both consumer and merchant sides to capture incremental value and margin expansion.

- The shift toward value-added services (branded checkout, merchant solutions, cross-border payments, crypto) offers higher margins and longer-term monetization.

- Progress in emerging digital commerce channels (mobile wallet, in-app payments, generative-AI commerce integration) may unlock new growth avenues and differentiate the platform further.

10. Bear Case

- Growth is decelerating in many developed markets, and PayPal faces significant competition from incumbents and agile fintechs, which may compress margins and limit upside.

- The business is somewhat mature and reliant on incremental improvements rather than large leaps, which may disappoint growth-oriented investors.

- Regulatory risks, fraud/loss exposure, macroeconomic headwinds (consumer spending softness) and currency fluctuations pose ongoing challenges to profitability and growth.

The stock is in a stage 1 consolidation and range bound on the monthly and weekly charts though the range is large ($45 – $101). It should stay in that range for the foreseeable future. The daily chart is range bound stage 1 as well between $65 – $77.