Grab Holdings is a Singapore-based technology company that has built a “super-app” in Southeast Asia, offering ride-hailing, food and grocery delivery, and digital financial services. It operates across multiple countries (including Singapore, Malaysia, Indonesia, the Philippines, Thailand, Vietnam and Cambodia) and aims to empower consumers and merchants with one unified platform. The company’s mission is to drive economic empowerment for everyone in the region. As the business matures, it is increasingly focused on becoming profitable and generating free cash flow rather than just growth. Grab went public via a SPAC merger in December 2021 and is now listed in the U.S. on the NASDAQ under ticker GRAB.

Most Recent Earnings (Q3 2025)

Grab reported its Q3 2025 results on November 3, 2025, generating approximately US$873 million in revenue, which narrowly beat analysts’ expectations (~US$872.9 million). The company also raised its full-year revenue guidance to between US$3.38 billion and US$3.40 billion, and lifted adjusted EBITDA guidance to US$490–500 million. While the deliveries segment revenue (US$465 million) was slightly below estimates (~US$470 million), the overall performance was solid thanks to improved user engagement and upsell from budget to premium offerings.

Founding, Products & Key Competitors

Grab was founded in 2012 (initially as MyTeksi) by Anthony Tan and Tan Hooi Ling in Malaysia, before rebranding to Grab and expanding throughout Southeast Asia. Over the years, the company has raised multiple funding rounds (with investors including SoftBank, Toyota, Microsoft and others) to support rapid growth across mobility, deliveries, and fintech. Key product lines include ride-hailing, food/grocery delivery, digital payments/financial services (loans, insurance, “Buy Now Pay Later”), and increasingly mapping & enterprise services (via GrabMaps). Grab’s headquarters is in One-North, Singapore.

Major competitors include regional players like GoTo Group (Indonesia), Sea Group (via Shopee’s delivery & logistics) and other global-local hybrids (Uber’s partnership footprints, food-delivery firms).

Market & Growth Outlook

Grab operates in the large and fast-growing Southeast Asia mobility + deliveries + fintech market. The ride-hailing market remains under-penetrated versus mature markets, and delivery and fintech services in the region are expected to see strong growth due to rising urbanization, smartphone/internet penetration, digital payments adoption, and consumer demand for convenience. According to data, Grab’s revenues have been growing at ~33% per year in recent years.

Looking forward to 2030, the total addressable market (TAM) for super-apps and embedded financial services across Southeast Asia could grow at a double-digit CAGR (perhaps ~15-25% depending on segment) driven by secular tailwinds (digitalization, increasing discretionary income, smaller players consolidating). The company’s emphasis on expanding into adjacent segments (e.g., mapping enterprise services, autonomous mobility) suggests optionality beyond the core mobility/delivery market.

Competitors Overview

GoTo Group (Indonesia) is a key competitor, especially in food delivery and ride-hailing. GoTo recently reported its first annual profit and remains open to consolidation with Grab. Sea Group (Singapore) offers logistics/delivery services in Southeast Asia and competes in e-commerce adjacency. Grab’s competition presents margin pressure (especially in delivery) and increasing complexity as players expand fintech offerings, which requires heavy investment and regulatory navigation.

Unique Differentiation

Grab’s unique differentiation lies in its super-app strategy: rather than being only a ride-hailing company, it spans mobility, deliveries, financial services and more. This allows it to cross-sell services, increase customer lifetime value, and build network effects across multiple service verticals. Furthermore, Grab’s regional footprint gives it scale in Southeast Asia, combined with localized expertise (drivers, partners, regulatory relationships) that newer entrants may find hard to replicate. Its push into mapping/enterprise services (GrabMaps) adds another layer of differentiation beyond peer focus on core delivery/mobility.

Management Team

- Anthony Tan — Co-Founder and CEO/Chairman. He steers the strategic vision, regional expansion and partnerships.

- Peter Oey — Chief Financial Officer, responsible for financial strategy, profitability turnaround and capital allocation (noted in recent earnings commentary).

- Philipp Kandal — Chief Product Officer (responsible for product innovation including GrabMaps and AI efforts).

Financial Performance (Last 5 Years)

Over the past five years, Grab has grown revenue at an estimated ~33% per annum (based on metrics pointing to ~33% CAGR). For example, in 2024 revenue was ~$2.80 billion, up ~18.6% from ~$2.36 billion in 2023. Earnings (net income) have improved: Grab reported a loss of ~$105 million in 2024, which was a significant improvement vs. prior years. On the balance sheet side, the company has been investing in scale and has achieved positive adjusted EBITDA guidance (raised in Q3 2025 to US$490-500 million) indicating improving profitability and potential free-cash-flow generation. While net margins remain thin (Simply Wall St reports net margin ~3.6%) the trajectory is positive. The shift from loss-making to near or break-even (and raising profitability guidance) is a key inflection.

Bull Case

- Grab’s super-app model offers multiple revenue engines (mobility + delivery + fintech + enterprise mapping) which could drive high revenue growth and margin expansion.

- Southeast Asia remains under-penetrated for many of these services; Grab’s scale and local knowledge give it a competitive edge across markets.

- Improvement in profitability (adjusted EBITDA up, cost discipline, raising guidance) could drive sentiment, valuation re-rating and free-cash-flow generation.

Bear Case

- Intense competition in mobility and delivery segments (price wars, subsidy wars) may continue to pressure margins and delay profitability.

- Regulatory, economic and execution risks in emerging markets (macro weakness, regulatory oversight, driver/labor issues) could derail growth.

- While diversification is promising (e.g., mapping services) these new segments may take many years to scale meaningfully; if core segments stall, the valuation may suffer.

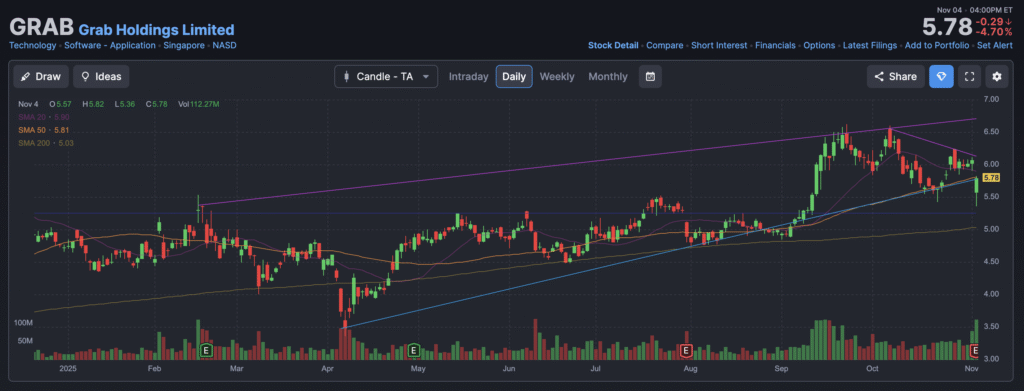

The stock is in a stage 1 consolidation on the monthly and weekly charts. The daily chart is in a bearish stage 3 markdown with support at $5.2 range where it might reverse. Until then we are still not interested.