Overview

United Parcel Service, Inc. (UPS) is a global logistics and package-delivery company that offers ground, air, freight, and supply-chain services in more than 200 countries and territories. In 2024 it reported total revenue of approximately $91.1 billion. UPS is headquartered in Atlanta, Georgia and operates one of the largest fleets of alternative-fuel vehicles and its own air cargo network. Its top competitors include FedEx Corporation (FedEx), DHL Group (DHL) and United States Postal Service (USPS). UPS’s core business lies in time-definite parcel delivery combined with broader supply-chain solutions.

Most Recent Earnings (Q3 2025)

For the quarter ended September 30, 2025, UPS reported adjusted earnings per share of $1.74 which exceeded analyst expectations of about $1.30. Revenue for the quarter came in at approximately $21.41 billion, above forecasts around $20.83 billion. The company also provided a forward-looking outlook: revenue for Q4 is projected at around $24 billion, slightly above analyst estimates of $23.8 billion. These results reflect improvements in pricing, cost control and network restructuring even though volume pressures remain. The guidance signals management is cautiously optimistic about holiday season demand and margin improvement.

Company History & Products, Founders & Key Competitors

UPS traces its roots back to 1907 when a young entrepreneur founded a messenger service in Seattle with a $100 loan. The company later adopted the name United Parcel Service in 1919 and over decades expanded from local courier work into national parcel delivery and global logistics. Today UPS provides a wide array of services: domestic and international parcel delivery (air and ground), supply-chain and contract logistics, freight forwarding (air, ocean, ground), customs brokerage and e-commerce fulfilment. Its headquarters remains at 55 Glenlake Pkwy NE, Atlanta, Georgia. The key competitors are FedEx, DHL and, to some extent, USPS in the U.S. parcel market. UPS competes on network reach, service reliability, pricing power and operational efficiency.

Market & Growth Outlook

UPS operates in the global logistics and parcel-delivery market—a market shaped by e-commerce growth, cross-border shipping demand, supply-chain complexity and pricing pressure. Analysts expect the global parcel & express market and broader logistics services to grow significantly through 2030, driven by e-commerce adoption, international trade flows and near-shoring/resiliency efforts. While specific CAGR figures for UPS’s sub-markets vary, many industry forecasts suggest high single-digit to low double-digit annual growth for express parcel delivery and supply-chain logistics through 2030. This presents a favorable structural backdrop for UPS, though macroeconomic headwinds (trade tariffs, volume softness) remain risks.

Competitors

UPS’s main competitor is FedEx, which competes across ground, air and freight segments. DHL is another major global competitor, especially in international express and logistics. In the U.S., USPS also competes in some parcel segments (especially lower-cost, high-volume ground shipments). Each competitor has its strengths: FedEx with strong air network, DHL with international reach, USPS with domestic low-cost access. UPS differentiates through its integrated network, alternative-fuel fleet, deep air/groud infrastructure and cost-saving initiatives aimed at improving margins.

Unique Differentiation

UPS differentiates itself through its vast integrated air-and-ground network, strong global reach (over 200 countries/territories), a large fleet of alternative-fuel vehicles and its own airline operations (via UPS Airlines). Its branding (“Customer First. People Led. Innovation Driven.”) emphasizes service, operational efficiency and innovation. The company’s network scale and vertical integration provide competitive advantage in offering time-definite delivery, complex logistics solutions and premium services. Its cost-reduction programs and pricing power also help support margin resilience in a challenging volume environment.

Management Team

UPS is led by CEO Carol B. Tomé, who previously had leadership roles at The Home Depot and joined UPS in 2020. Under her leadership the company has emphasized network restructuring and margin improvement. The CFO is Brian Dykes, responsible for financial strategy, cost-savings initiatives and capital allocation. Another key executive is Gwynne Stewart (Chief Commercial Officer), who oversees global sales, marketing and customer operations. Together they are driving UPS’s transformation efforts amid evolving logistics dynamics.

Financial Performance (Last 5 Years)

Over the past five years UPS’s revenue growth has been modest to negative in some years. For example, revenue decreased slightly in 2025 Q1 compared to a year ago, with Q1 2025 revenue of $21.5 billion down 0.7% from Q1 2024. UPS’s earnings per share has grown in some quarters (e.g., Q1 2025 non-GAAP EPS of $1.49 up about 4.2% vs year-ago). The company’s business has been impacted by global trade shifts (tariffs, China-U.S. flows), volume softness and freight declines, which has compressed growth. On the balance sheet, UPS holds a large asset base given its network, aircraft, vehicles and facilities; the company continues to invest in automation and alternative fuel vehicles while managing debt levels and returning capital via dividends (it has a long dividend increase streak). The cost-savings program (targeting $3.5 billion in annual savings in 2025) is a key lever for improving earnings growth going forward. While revenue growth has been challenged, UPS is leveraging operational improvements and pricing to boost margins. If the company succeeds in restructuring and better aligning capacity with demand, future earnings growth may accelerate even if revenue growth remains modest.

Bull Case

- UPS’s cost-savings and network-restructuring efforts (targeting ~$3.5 billion in 2025) could significantly boost margins and earnings power if executed well.

- Strong pricing power and global reach enable UPS to capture value in the growing e-commerce and cross-border parcel markets.

- Its investment in alternative-fuel fleet and logistics infrastructure positions it well for sustainable growth and differentiation in a green/efficient world.

Bear Case

- Continued volume declines or softness in business-to-business shipping could pressure revenue growth and margins.

- Risks from global trade disruptions, tariffs and macroeconomic slowdown remain significant for a logistics company operating globally.

- Execution risk: cost-savings and restructuring programs are complex; if they don’t deliver as expected, margins may lag and investor confidence may suffer.

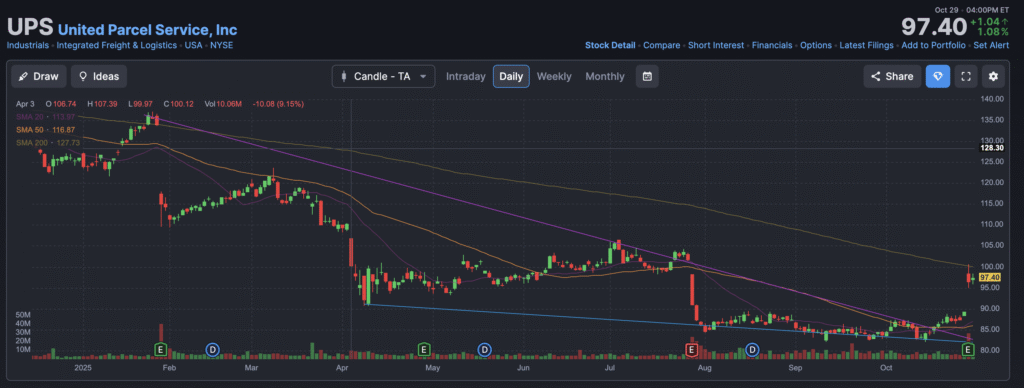

The stock is in a bearish stage 4 markdown on all 3 time frames, but is reversing in the $82 range, which could signal a move higher and consolidate in the $106 range as well. The near term outlook is more consolidation to the $106 and lower.